Meet Ergin, a 32-year-old software developer from Tirana. Every day, he codes for two companies based in Germany and Denmark. He sends invoices, receives payments, and everything seems perfectly fine—or so he thinks. Every Monday and Friday, his earnings arrive consistently in his personal bank account. He hasn't registered a business, has no Tax ID (NIPT), and doesn’t employ an accountant. "I don’t need one," Ergin claims, "the law says 0% tax until 2029."

Ergin is right about the 0% tax rate, but he is dead wrong about how he collects his income. And this single mistake will cost him 15% of his total revenue, without the possibility of deducting a single expense.

This article is written specifically for people like Ergin: Albanian professionals working as freelancers for international clients—software developers, designers, consultants, marketers, lawyers, and architects—who are still unsure about their tax obligations. If you find yourself in this situation, reading this guide in full could save you tens of thousands of dollars and protect you from tax risks that many professionals don't even know exist.

Who is this article for?

This article is addressed to individuals providing professional services to clients outside of Albania, whether they are foreign companies or non-resident individuals. Typically, this includes professionals who receive payments primarily or entirely from international sources, those who have not yet registered a business in Albania, or those who have registered but are not channeling their income correctly, and whose annual income is below 14 million ALL (approximately $140,000 USD).

This category is broad and growing. The globalization of the labor market and the rise of international platforms like Upwork, Toptal, Fiverr, and many others have allowed many Albanian professionals to serve global clients without the need to emigrate. While this is a positive development, it also brings specific tax obligations that cannot be ignored.

If you are in this situation, reading this article in full could save you tens of thousands of dollars and protect you from tax risks that many professionals aren’t even aware exist.

Defining the "Freelancer?

The term"freelancer"is widely used in everyday language, on international work platforms, and in professional communication; however, it has no legal definition in Albanian legislation. Law No. 29/2023 "On Income Tax" does not use this term at all. Instead, Article 2 of this law defines the concept of a "Self-Employed Individual" as any natural person engaged in the supply of any type of service or engaged in other professional activities, distinct from commercial activities.

When we refer to freelancers in this article, we are specifically referring to this legal category: self-employed individuals who provide professional services independently, usually for more than one client, without being in an employment relationship with them. This distinction between the popular and legal term has practical importance: the Albanian tax system does not treat you as a "freelancer," but as a Sole Proprietor (Self-Employed Individual), and all obligations, benefits, and deadlines described here stem from this legal status.

The Common Mistake: Collecting Payments in Personal Accounts

Why does this mistake happen?

It is understandable why this situation is so common. Many Albanian freelancers have correctly heard that Law No. 29/2023 "On Income Tax""(Article 69, Point 1, Letter “dh”) provides for a 0% profit tax rate for self-employed individuals with gross income up to 14 million ALL per year, and that this favorable rate applies until December 31, 2029. This is absolutely true.

However, two incorrect conclusions are often drawn from this fact. The first is: "I have no tax obligation, so I don't need to open a business." The second is: "I can collect payments anywhere; the only condition is the amount, not the form."

The 0% rate is not automatic or universal. It applies only when all the proper conditions for registration and income channeling are met.

What exactly happens when you collect payments without a Tax ID (NIPT)?

When payments from foreign clients arrive in your personal bank account and you are not registered as a Sole Proprietor with a NIPT, the tax administration treats these amounts as informal personal income. Based on Articles 58 and 59 of Law No. 29/2023,undeclared income is subject to a 15% tax on the total gross amount, without deducting any expenses: no office rent, no computers, no software, no professional subscriptions, no business travel—nothing.

Concretely: if you received $50,000 USD from foreign clients during 2025 into your personal account, your potential tax exposure is $7,500 USD. Furthermore, if discovered by the tax authorities, this amount comes with administrative fines and interest for late payment according to current tax legislation.

Why the risk is increasing year after year?

Since 2020, Albania has implemented the international Common Reporting Standard (CRS),which enables the automatic exchange of banking information between the tax authorities of member countries. This means that information regarding international bank transfers is increasingly accessible to the Albanian tax administration. Those who have waited to "slip through" the cracks risk facing situations that would have been much easier to address a few years ago.

The 0% Tax Rate until 2029: Only if You Meet the Criteria

The 0% tax rate for self-employed individuals with income up to 14 million ALL (approx. $150,000 EUR or $170,000 USD at current rates) per year is one of the most favorable tax provisions in the history of Albanian legislation. But it does not activate itself. It requires three specific and cumulative conditions, all of which must be met simultaneously.

Condition 1: Registration as a Sole Proprietor (NIPT)

The NIPT (Tax Identification Number) is your tax identity as a business entity. Registration is done through the National Business Center (QKB) via the e-Albania portal, with no administrative costs and usually within 1 to 2 business days. This step is mandatory: without a NIPT, none of the other tax advantages can be applied.

Read also [Initial Registration of a Sole Proprietor].

Condition 2: Business Bank Account

Immediately after obtaining your NIPT, you must open a bank account in the name of the NIPT and ensure that all payments from foreign clients arrive in this specific account, not your personal one. This distinction is not a legal formality without consequences; it is the basis upon which the tax administration determines whether the income is treated as business income (at a 0% rate) or informal personal income (at a 15% rate on the gross).

Read also [10 Steps to Follow After Initial Registration].

Condition 3: Income Thresholds

Annual gross income must not exceed 14 million ALL (approx. $170,000 USD). If this limit is exceeded, the profit tax rate becomes 15% according to the progressive scale of Article 24, Point 2, of Law No. 29/2023 for the amount exceeding 14 million ALL.

When all three conditions are met simultaneously, you have the right to apply the 0% rate on taxable profit. This means that even if you earned $60,000, $80,000, or $100,000 USD in a year, if you are correctly registered and maintain proper accounting, your profit tax until December 31, 2029, is zero.

The Advantage of Foreign Clients under the Law

The 80% and 90% Rule: What it is and why it matters

Law No. 29/2023contains a specific provision that many Albanian freelancers are unaware of, yet it affects them directly. Article 12, Point 1, Letter “ç” stipulates that the income of a self-employed individual can be reclassified as “employment income” if one of the following two conditions is met:

80% or more of the income is derived from a single client; OR 90% or more of the total income is derived from no more than two clients.

Reclassification as an “employee” has significant tax implications, as employment income is subject to progressive personal income tax under Article 24, Point 1, of Law No. 29/2023, and does not benefit from the 0% rate intended for small businesses.

Read also [Annual Tax Base and Tax Rates for Individuals]

Why is this important for freelancers? Because many work with one or two major clients and have no need to diversify. This is perfectly normal in the international professional services market. Without the protective provision explained below, these individuals would risk reclassification regardless of how well they have organized their work.

Explicit Protections for International Service Providers

A paragraph added by Law No. 81/2025, dated 11.12.2025, following sub-items “i” and “ii” of Letter “ç” of Article 12, Point 1, explicitly states: “Letter ‘ç’ does not apply if the self-employed individual provides services solely to persons who are non-residents of the Republic of Albania or solely to entities that do not have a permanent establishment in the Republic of Albania. In this case, the self-employed individual is considered to generate business income.”

In simple terms: If all your clients are outside of Albania, the 80% and 90% rule does not affect you at all. You are automatically considered a person generating business income, not employment income, regardless of the number or concentration of your clients.

The Legislator’s Intent

This provision is not a technical legal accident. It is a deliberate measure by the Albanian legislator to encourage local professionals to stay and work from Albania while serving the international market. The logic is clear: any Albanian professional who earns money from abroad and spends or invests it locally contributes to the national economy. The state recognizes this reality and does not wish to penalize it.

Conversely, if your clients were primarily Albanian companies, the risk of reclassification would be real. In that case, you would either need to diversify your client base or complete the “Self-Employed Status Declaration” (Annex 1 of Law No. 29/2023), which is submitted by March of the tax year.

When are you obligated to file the DIVA (Annual Tax Return)?

Three Legal Requirements

The DIVA (Annual Personal Income Tax Return) is the annual filing that every individual is obligated to submit if they meet at least one of the three conditions provided by Article 67 of Law No. 29/2023:

Condition 1: Your annual taxable income from all sources exceeds 1,200,000 ALL (approximately $12,000 USD) per year. Practically, every freelancer with foreign clients earning over one thousand dollars a month automatically meets this threshold.

Condition 2: You are simultaneously in an employment relationship with more than one employer, regardless of the income amount. This is of particular importance to those who work both as salaried employees under an employment contract and as freelancers, as the combination of these two statuses automatically triggers the DIVA obligation.

Condition 3: You have other income not subject to final withholding tax that exceeds 50,000 ALL (approximately $500 USD) per year. This threshold is very low and practically any additional income triggers it.

Read More about the taxes paid by individuals.

The Critical Difference: With NIPT vs. Without NIPT

If you are not registered as a sole proprietor (NIPT) and you file the DIVA, your income from foreign clients will be taxed as personal income at a 15% rate on the total gross amount, without any deductible expenses.

If you are registered as a sole proprietor (NIPT) and your income is below 14 million ALL, your profit tax is 0% until 2029. At the same time, you have the right to deduct documented business expenses—computers, software, professional subscriptions, internet, office rent, business travel, and any other expense related to your activity—thereby lowering the tax base even for the period after the 0% rate expires in 2029.

The DIVA is submitted every year no later than March 31st of the following year. Your accountant manages this process, but the legal obligation remains yours personally.

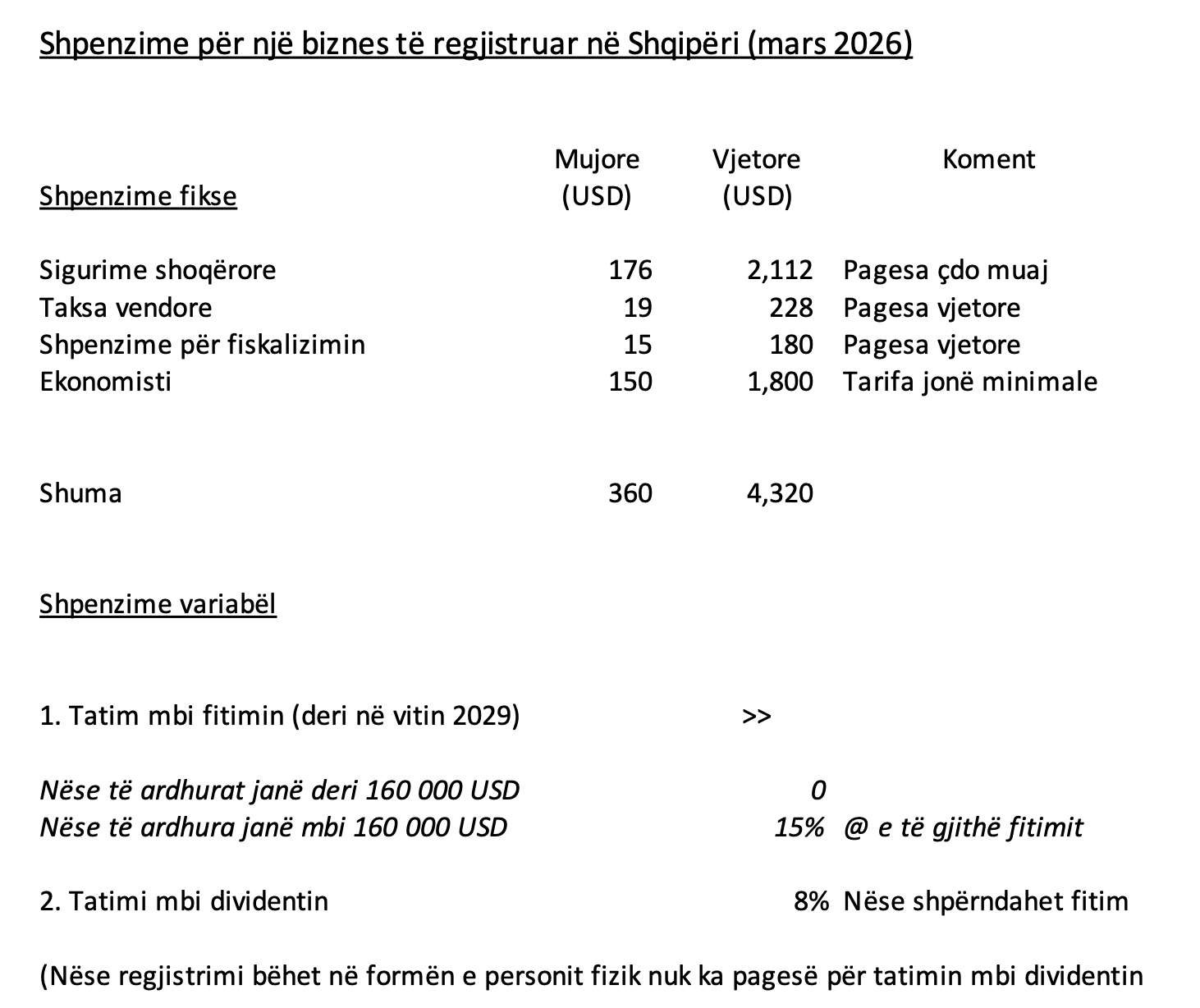

The Costs of Registering as a Sole Proprietor

What the real cost includes

Registering as a sole proprietor (NIPT) is not free from an operational standpoint. There are fixed monthly and annual costs that must be carefully planned. Based on our updated data as of March 2026, the typical expenditure breakdown is as follows:

Social and health insurance are mandatory monthly costs amounting to $176 USD per month, or $2,112 USD per year. This contribution is not just a legal obligation: it ensures your access to the public pension and healthcare system.

Local municipal tax is an annual cost that breaks down to $19 USD per month, or $228 USD per year. It is paid to the municipality where you have registered your activity and is non-negotiable.

Fiscalization certificate and software cost $15 USD per month, or $180 USD per year. The fiscalization system is mandatory and ensures the real-time electronic issuance of invoices as required by Albanian legislation.

External accountant, at our minimum rate, costs $150 USD per month, or $1,800 USD per year. This expense covers bookkeeping, the preparation and submission of tax declarations, invoice registration, as well as ongoing tax consultancy throughout the year.

The total fixed expenses are approximately $360 USD per month, or $4,320 USD per year, based on our standard fee.

What is excluded: Variable Expenses

Variable expenses are highly favorable. As explained, the profit tax is 0% for gross income up to 14 million ALL. The 8% dividend tax only applies if you distribute profit from your business account to your personal account.

However, if you register as a Sole Proprietor (Person Fizik) and not as a Limited Liability Company (sh.p.k.), the dividend tax does not apply at all. This is because the legal form of a Sole Proprietor does not provide for profit distribution as a dividend; income is withdrawn directly.

Calculating the Break-even Point: When is registration worth it?

The Simple Math

The central economic question many freelancers ask is this: at what income level does it make financial sense to register as a Sole Proprietor, considering the annual fixed costs?

The calculation is straightforward. With annual fixed costs of $4,320 USD and an alternative tax of 15% on gross income without a NIPT, the break-even point is found by dividing the fixed costs by the tax rate: $4,320 / 0.15 = $28,800 USD per year.

This means: If your annual income from foreign clients is above approximately $29,000 USD, registering as a Sole Proprietor with a fixed cost of $4,320 per year is financially more favorable than paying the 15% tax without a NIPT. Below this threshold, from a purely immediate economic standpoint, the 15% tax is slightly lower than the fixed costs. However, this comparison ignores two critical factors: the legal obligation, which exists regardless of the amount, and the cumulative risk of remaining unregistered over several years.

The Hidden Long-term Advantage

This comparison only considers the current 0% rate valid until 2029. After this date, having a NIPT grants you the right to deduct expenses from your tax base, which significantly lowers your effective tax. Without a NIPT, the 15% tax on gross income allows for no deductions. Therefore, the long-term advantage of registration is even greater than what the current simple calculation suggests.

Real-number Scenarios: With NIPT vs. Without NIPT

Let’s examine the specific financial consequences of both paths for various annual income levels, directly comparing the tax incurred without a NIPT against the fixed operational costs with a NIPT.

If you have $20,000 per year: Without NIPT, you pay $3,000 in tax (15% x 20,000), while with NIPT, you have $4,320 in fixed costs and $0 in tax. The difference is $1,320 in favor of the option without NIPT, but you are legally unregistered and create a cumulative risk.

If you have $29,000 per year: Without NIPT, you pay $4,350 in tax, while with NIPT, you have $4,320 in fixed costs and $0 in tax. The difference is practically zero, and registration grants you full legal protection.

If you have $30,000 per year: Without NIPT, you pay $4,500 in tax, while with NIPT, you have $4,320 in fixed costs and $0 in tax. You save $180 and are in full compliance with the law.

If you have $50,000 per year: Without NIPT, you pay $7,500 in tax, while with NIPT, you have $4,320 in fixed costs and $0 in tax. You save $3,180 every year, alongside legal protection.

If you have $80,000 per year: Without NIPT, you pay $12,000 in tax, while with NIPT, you have $4,320 in fixed costs and $0 in tax. You save $7,680 per year.

If you have $120,000 per year: Without NIPT, you pay $18,000 in tax, while with NIPT, you have $4,320 in fixed costs and $0 in tax. You save $13,680 every year.

| Annual Income (USD) | Tax without NIPT (15%) | Costs with NIPT (USD) | Annual Savings (USD) |

|---|---|---|---|

| 15,000 | 2,250 | 4,320 | -2,070 |

| 20,000 | 3,000 | 4,320 | -1,320 |

| 29,000 | 4,350 | 4,320 | +30 |

| 30,000 | 4,500 | 4,320 | +180 |

| 40,000 | 6,000 | 4,320 | +1,680 |

| 50,000 | 7,500 | 4,320 | +3,180 |

| 80,000 | 12,000 | 4,320 | +7,680 |

| 120,000 | 18,000 | 4,320 | +13,680 |

Note: The table calculates only the profit tax. With a NIPT, business expenses such as software, equipment, internet, consultancy, and any other documented expenses are deductible, which lowers the tax base even after the 0% rate expires in 2030.

What about past years? The 2026 Fiscal Amnesty

What is Fiscal Amnesty?

Many freelancers reading this article already have years of activity without registration. The natural question is whether there is a way out and what happens to the income from previous years.

Law No. 86/2025“On the waiver, termination, and payment of tax obligations to the central and local tax administration”entered into force on January 1, 2026, and expires on December 31, 2026. This law is otherwise known as Fiscal Amnesty or Fiscal Peace, and it offers a rare window of pardon structured by time periods.

Read also Fiscal Amnesty 2026: Which Tax Obligations Are Waived and How You Can Benefit?

Obligations incurred before December 31, 2014

The primary tax debt, fines, and late interest are all fully and automatically waived. You have nothing to pay for this period. Social and health insurance contributions for this period are also waived.

Obligations from January 1, 2015, to December 31, 2019

These are handled via two options: Option 1 (Fast-track Option): Allows you to pay 50% of the principal tax amount by June 30, 2026. In exchange, the remaining 50% of the principal plus 100% of fines and late interest are waived. Option 2 (Installment Option): Allows you to pay 75% of the principal amount in installments until December 31, 2026. In exchange, the remaining 25% of the principal plus 100% of fines and late interest are waived. Note: Insurance contributions for this period must be paid in full, but fines and late interest are waived.

Obligations from January 1, 2020, to December 31, 2024

Payment of 100% of the principal tax amount is required by December 31, 2026. In exchange, 100% of the fines and late interest are fully waived. Insurance contributions for this period must be paid in full, but fines and late interest are waived.

A Concrete Example

If you collected $40,000 USD from foreign clients during 2023 without being registered, the theoretical tax liability would be $6,000 USD (15% of the gross amount). Under the amnesty, if you pay the principal amount by December 31, 2026, all fines and late interest are fully waived. Additionally, the insurance contributions for the period in question must be addressed.

Who is ineligible?

The amnesty does not apply to taxpayers with final criminal convictions for tax evasion, those under active criminal investigation, or those with active court or administrative cases, unless they choose to withdraw them voluntarily.

The window for amnesty closes on December 31, 2026. Based on official government statements, this is expected to be the final round of tax pardons before tax enforcement is further tightened.

Actionable Steps: What you should do today

If, after reading this article, you have decided to regularize your tax situation, the path is clear and achievable in a few steps.

Step 1: Contact a specialized accountant to conduct an assessment of your specific situation: years of activity, total collection amounts, existing documentation, and any historical liabilities. This assessment gives you a complete overview before taking any action.

Step 2: Register as a Sole Proprietor (NIPT) through the e-Albania portal. The process has no administrative costs and is usually completed within 1 to 2 business days. Your accountant can fully manage this process on your behalf.

Step 3: Open a business bank account and notify your international clients to transfer future payments specifically to that account. This step must be taken immediately after obtaining the NIPT.

Step 4: If you have years of activity without registration, evaluate the possibility and magnitude of historical liabilities. The accountant will accurately calculate the amounts and show you how to benefit from Law No. 86/2025 before it expires.

Step 5: Establish a continuous accounting system: configure the fiscalization software, maintain accounting books, and document every invoice and collection according to legal requirements. From this point forward, your accountant ensures that everything is in order every month and every year.

Frequently Asked Questions (FAQ)

Should I open a business even if I earn very little, say under $20,000 USD per year?

Yes. If you carry out continuous economic activity, the legal obligation to register exists regardless of the income level. The immediate economic question (when it is financially worth it) is different from the legal question (when you are obligated). Between $20,000 and $29,000 USD, the financial advantage becomes clear, but the legal obligation begins the moment the activity starts.

My clients are all outside of Albania. Do I have any specific advantage?

Yes, exactly as explained in the section "The Advantage of Foreign Clients under the Law." The reclassification rule as an employee (80% or 90% of income from few clients) does not apply if your clients are non-residents or do not have a permanent establishment in Albania. This protection is explicitly provided by Law No. 81/2025 and applies automatically, without the need to submit any additional declarations.

Do I need to issue invoices even for clients abroad?

Yes. Every collection must be documented with a proper invoice issued through the fiscalization system. Invoices for services to non-residents have a 0% VAT rate if your turnover does not exceed the VAT registration threshold (10 million ALL, approx. $100,000 USD). The fiscalization system issues the invoice electronically regardless of the client's location.

I am registered as a Sole Proprietor but payments still arrive in my personal account. What should I do?

Act immediately: notify your clients to transfer future payments to the NIPT account. Meanwhile, consult with your accountant regarding the accounting and documentary treatment of payments that arrived mistakenly in the personal account. There are mechanisms in place to address this situation without exposure to sanctions.

The 0% rate ends after 2029. What happens then?

After December 31, 2029, the profit tax returns to the standard rate of 15% on net profit for income up to 14 million ALL, and 23% for amounts exceeding this limit. However, with a NIPT, you will have the right to deduct all documented business expenses from the tax base, which significantly lowers the effective tax. Without a NIPT, the 15% tax is applied to the total gross amount, without any deductions or optimization possibilities.

Until when can I benefit from the fiscal amnesty?

The deadline is December 31, 2026. After this date, historical liabilities will be treated with the full tax rate plus fines and late interest according to tax legislation. The process of assessment, documentation, and payment takes time and planning, so it is recommended to start as soon as possible.

Register and Stay Protected

Albanian law has given freelance professionals with international clients a rare combination of advantages: a 0% tax rate until 2029, protection from reclassification as an employee, favorable treatment of foreign income, and an amnesty window for regularizing past years. However, all these advantages have a single condition: to be correctly registered.

The mistake of collecting payments in a personal account is justified neither by ignorance of the law nor by the fact that no one has checked yet. The Albanian tax administration has increasingly broad access to banking information and has intensified data cross-referencing in recent years.

If you are ready to regularize your situation, contact the AlProfit Consult team. We offer an initial consultation where we will assess your specific position, tell you exactly what needs to be done, and support you in every step of the process—from registration to the submission of annual declarations.

This article is for informational purposes only and does not constitute individual tax advice. Every specific situation must be evaluated by a licensed expert. AlProfit Consult is not responsible for decisions made solely based on this article without prior professional consultation.