Law No. 85/2025 “On the Revaluation of Immovable Property” entered into force in January 2026. However, the mere adoption of the law was not sufficient to start the process. The procedures were not clear, the forms did not officially exist, the service fees had not been published, and no Cadastre office could process any application without the implementing instruction. This situation created uncertainty and led many property owners to wait before taking action.

The Joint Instruction No. 5, dated 19 February 2026, signed by the Minister of Finance and the Director General of ASHK, closed this gap. The full document, with all subpoints, annexes, and tables, provided what had been missing: precise calculation rules, the official forms (Annexes 1–4), the service fees, ASHK’s time limits, the procedure for refunding incorrect payments, and the necessary clarifications for special cases such as properties with no registered value.

This blog does not aim to re-explain from the beginning why revaluation is worthwhile for tax purposes or how the 5% versus 15% calculation works—we have addressed that extensively in our guide published in January 2026. The purpose here is to explain precisely what this new Instruction introduced, how the situation changed before and after 19 February, and what you should specifically do now.

What was unclear before the instruction and what it clarified

If you had asked an ASHK employee in early February 2026 how to apply for revaluation, you would have received an uncertain answer: “The law exists, but we are waiting for the instruction.” This was not an administrative problem; it was a legal one. Without implementing instructions, no procedure had a legal basis to be processed. That is why ASHK offices were not accepting applications, even if the owner showed up with all documents.

Udhëzimi Nr. 5/2026 (hyrë në fuqi 19 shkurt 2026) i dha fund kësaj situate. Ja konkretisht çfarë nuk dihej dhe u sqarua:

The official service fee was not known

Before the instruction, owners did not know how much the administrative process would cost, beyond the 5% tax. The Instruction (Chapter VIII) publishes the full table with three fee levels based on the size of the tax, under the service code RVP.

The revaluation date had remained undefined

It was unclear whether the legally relevant date was the application date, the tax calculation date, or the payment date. The Instruction clarifies it without any doubt: the revaluation date is the date the tax is paid. This has direct implications—if you sell the property two months after revaluation, the sale basis is calculated from the value on the date you paid, not when you submitted the documents.

The forms did not officially exist

The Instruction attaches Annexes No. 1–4, which are respectively: the application form for individuals, the voluntary declaration for businesses, the invoice template, and the payment form for legal entities.

ASHK’s registration deadline had no legal basis

Now it is precise: 5 working days from the confirmation of payment. Before the instruction, this deadline did not exist and owners had no legal instrument to push ASHK to act.

Payment codes were not officially published

Individuals pay using revenue code 7020900, through ASHK’s special account at second-tier banks. Legal entities pay using code 7020400, directly at the Regional Tax Directorate.

The rule for properties with no value had remained unclear

Instruction 5/2026 explicitly refers to the formulas in Instruction 34/2023 and its Annex No. 1, specifying how the deductible value is found for each type of property with no registered value.

The procedure for refunding an erroneous payment was missing

Now Chapter VII of the Instruction regulates it precisely: the deadline, the competent authority, and the refund route.

How the tax base is calculated — the exact formula, depreciation deduction, and the case of the minimum fiscal price

Before we talk about the procedure, we need to understand how the tax is calculated in practice, because this directly affects your decision on whether to revalue and at what value.

The basic revaluation formula is:

Tax = (Revaluation Value − Deductible Value) × 5%

Where the “revaluation value” may be the minimum fiscal price according to ASHK or the value in a licensed private expert’s report, and the “deductible value” is the last registered value on which tax was paid (purchase, previous revaluation, inheritance with value, gift with value).

Path 1: Revaluation using fiscal prices through ASHK

When you choose for ASHK to do the calculation itself without a private expert, the revaluation value is calculated based on the minimum fiscal prices of buildings, according to Council of Ministers Decision (VKM) No. 132/2018 and its relationship with updated zone prices. But the reference price is not applied as-is—depreciation is deducted.

Depreciation of buildings

Each full year from the date you obtained ownership reduces the reference price by 1%. The maximum reduction is 30% and never exceeds this limit regardless of age. This deduction applies only to buildings, not to land.

Full formula for buildings:

Minimum fiscal revaluation price = Area (m²) × Zone reference price × [1 − (full years × 1%)], where the maximum deduction is 30%.

Example: an 85 m² apartment in Tirana, central zone; the zone reference price for 2026 is 150,000 ALL/m². Ownership was first acquired in 2003, i.e., 23 full years up to 2026. Registered purchase value: 3,200,000 ALL.

Zbritja e amortizimit: 23 × 1% = 23%.

Depreciation deduction: 23 × 1% = 23%.

Çmimi i korrigjuar: 150,000 × (1 − 0.23) = 115,500 lekë/m².

Adjusted price: 150,000 × (1 − 0.23) = 115,500 ALL/m².

Vlera e rivlerësimit: 85 × 115,500 = 9,817,500 lekë.

Revaluation value: 85 × 115,500 = 9,817,500 ALL.

Vlera e zbritshme (blerja 2003): 3,200,000 lekë.

Deductible value (purchase 2003): 3,200,000 ALL.

Baza tatimore: 9,817,500 − 3,200,000 = 6,617,500 lekë.

Tax base: 9,817,500 − 3,200,000 = 6,617,500 ALL.

Tatimi 5%: 330,875 lekë.

5% tax: 330,875 ALL.

Tarifa e shërbimit: 10,000 lekë (tatimi mbi 300,000 lekë).

Service fee: 10,000 ALL (tax over 300,000 ALL).

Kosto e plotë administrative: 340,875 lekë.

Total administrative cost: 340,875 ALL.If this apartment is sold without revaluation for 12,000,000 ALL, the sale tax would be: (12,000,000 − 3,200,000) × 15% = 1,320,000 ALL. Difference in favor of revaluation: 1,320,000 − 340,875 = 979,125 ALL in savings.

Path 2: Revaluation with a report by a licensed expert

This path has an explicit condition in Instruction 5/2026 that many owners overlook: the private expert’s report cannot state a value below the minimum fiscal price with depreciation applied. If the expert values the property below this threshold, ASHK rejects the report automatically and the process restarts. Therefore, the expert must know this limitation before starting the inspection.

Why choose an expert if there is a minimum? Because the real market value is often significantly above the minimum fiscal price, especially in dynamic areas such as Tirana, Durrës, Saranda, or the coast. If you revalue at the real market value, your new cost base will be close to the current market price, and capital gains tax when you sell will be minimal—because the difference between the sale price and your new base will be very small.

Example: if your property is worth 15,000,000 ALL today and you revalue it via an expert report at exactly 15,000,000 ALL, then if you sell tomorrow for 16,000,000 ALL you would pay 15% only on the 1,000,000 ALL difference—i.e., 150,000 ALL sale tax, very small compared to what you would pay without revaluation. Therefore, a private expert favors owners planning a short-term sale and seeking maximum tax savings.

Properties with no registered value — how the deductible value is found by property type

This has been among the most discussed points and the biggest source of confusion among our clients. Tens of thousands of properties in Albania have zero value or no value registered on the cadastral card—properties privatized under Law 7652/1992, properties obtained with an AMTP under Law 7501/1991, inherited properties without a notarial deed showing value, legalized properties. Instruction 5/2026, by referring to Instruction 34/2023 and its annexes, clarifies them with clear formulas depending on the property type.

Buildings with no purchase value

For buildings registered with no purchase value—such as those privatized under Law 7652, inherited with no value, or transferred free of charge through administrative acts—the deductible value is the utilization cost per square meter set by the National Housing Entity (EKB), according to the year the property was registered with the local cadastre directorate (DVASHK). So, if your home was officially registered in 2001, the EKB cost for 2001 is multiplied by the area and that is the deductible value.

Example: a 70 m² privatized apartment registered with DVASHK in 1999. The EKB utilization cost for 1999 according to the tables is 8,000 ALL/m². Deductible value: 70 × 8,000 = 560,000 ALL. If today’s minimum fiscal price (with 27 years of depreciation = 27% reduction) is 7,500,000 ALL, the tax base is 7,500,000 − 560,000 = 6,940,000 ALL and the 5% tax would be 347,000 ALL.

Land with no purchase value

For land acquired without a price—via AMTP, a court decision, or inheritance with no registered value—the formula changes. The deductible value is the current price according to the value map, divided by the inflation index for the year ownership was obtained. The inflation index table is found in Annex No. 1 of Instruction 34/2023 and covers the period from 1989 to 2023.

The logic is simple: since you paid nothing for the land, the deductible value is calculated by “rolling back” today’s market value in time, using inflation. This provides a reasonable base instead of zero—which would mean tax on 100% of the current value.

Shembull: tokë bujqësore 5,000 m², zonë periferike Fier, fituar me AMTP në vitin 1993. Çmimi sipas hartës së vlerave sot: 280 lekë/m². Vlera totale sipas hartës: 5,000 × 280 = 1,400,000 lekë. Indeksi i inflacionit për vitin 1993 sipas Aneksit 1: 4.250.

Vlera e zbritshme: 1,400,000 ÷ 4.250 = 329,412 lekë.

Baza tatimore: 1,400,000 − 329,412 = 1,070,588 lekë.

Tatimi 5%: 53,529 lekë.

Tarifa e shërbimit: 3,500 lekë (tatimi nën 150,000 lekë).

Totali: 57,029 lekë.Example: 5,000 m² agricultural land, peripheral area of Fier, acquired with AMTP in 1993. Current value-map price: 280 ALL/m². Total value per map: 5,000 × 280 = 1,400,000 ALL. Inflation index for 1993 per Annex 1: 4.250. Deductible value: 1,400,000 ÷ 4.250 = 329,412 ALL. Tax base: 1,400,000 − 329,412 = 1,070,588 ALL. 5% tax: 53,529 ALL. Service fee: 3,500 ALL (tax under 150,000 ALL). Total: 57,029 ALL. Compare: if the same land is sold without revaluation for 1,600,000 ALL, the 15% sale tax on gain would be: (1,600,000 − 329,412) × 15% = 190,588 ALL. Savings: 190,588 − 57,029 ≈ 133,000 ALL, almost 2.5 times the difference. And this without factoring in further price increases.

Properties privatized under Law 7652/1992 — the first apartments

This property type has special treatment under Instruction 34/2023, also confirmed by Instruction 5/2026. For the first sale of a privatized apartment (i.e., the original privatization owner sells for the first time), the minimum fiscal reference price is applied at 50%—meaning half the zone reference price is taken without applying depreciation. This privilege applies only to the first sale by the privatization owner.

If the apartment has already been sold and is now owned by the first buyer, this preferential treatment no longer applies. If that buyer wishes to revalue, the deductible value is their registered purchase price.

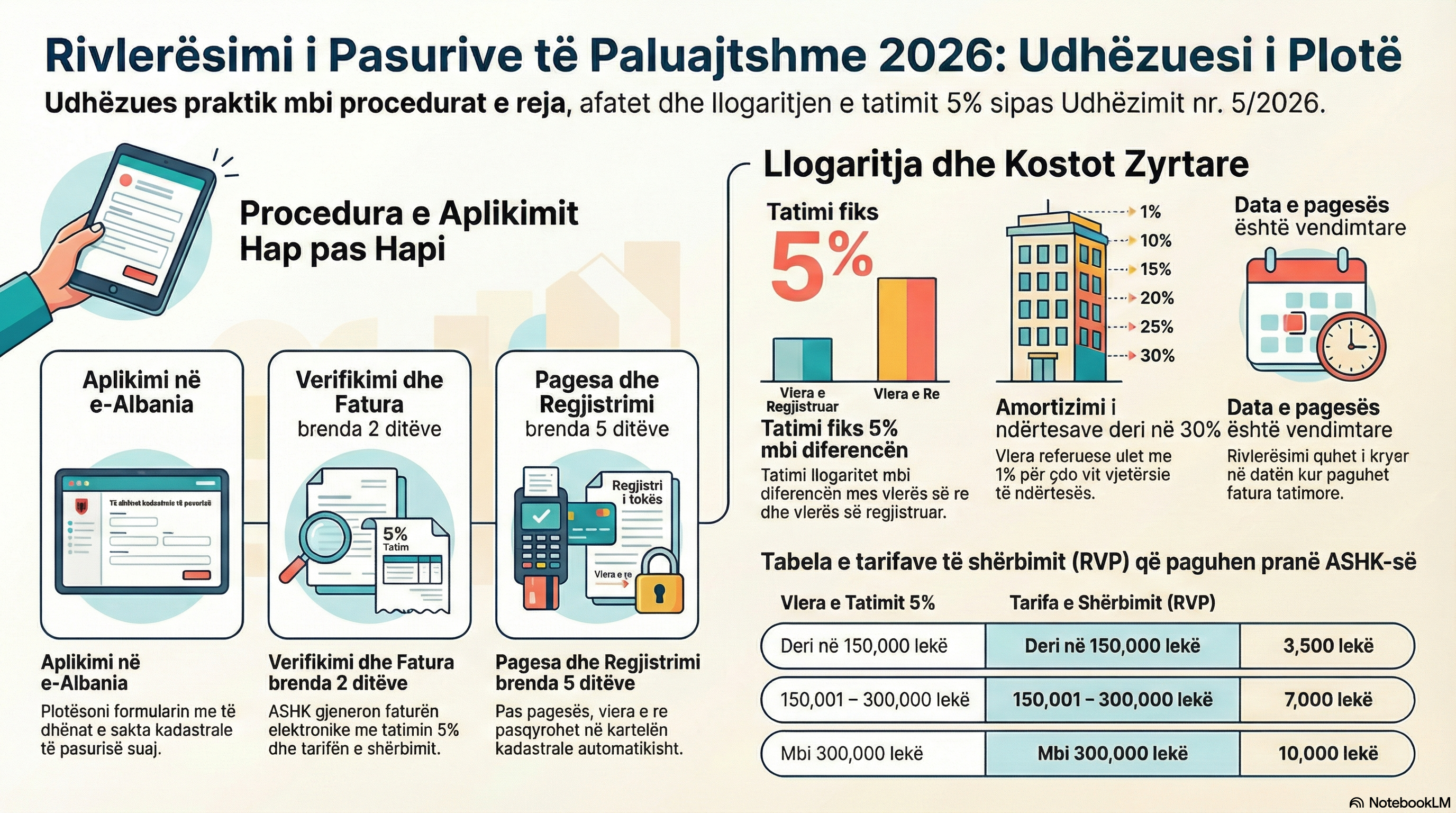

Step-by-step application procedure according to the instruction

Instruction 5/2026 (Chapters III and IV) structures the process into five consecutive steps, with clear deadlines for each phase.

Step 1: Application through e-Albania

An individual applies through the government portal e-Albania, completing the form according to Annex No. 1. The form must include: cadastral zone, property number, and the unique code ZK-Volume-Page. If the individual does not have these details, they may upload a scan of the ownership certificate and the ASHK employee identifies the property.

The application is addressed to the local ASHK directorate where the property is geographically located, not where the owner lives. Therefore, if you live in Tirana and the property is in Shkodra, the application goes to ASHK Shkodra.

Along with the application, you should also submit a request for a copy of the property card, because once the revaluation is finalized you will want the updated certificate with the new value. If it is done through a representative, the latter must have a valid power of attorney.

Step 2: ASHK verification and invoice generation within 2 working days

Within 2 working days of receiving the application, the ASHK employee performs two actions: verifies whether the applicant is a registered owner/co-owner and checks whether the property is correctly identified. If conditions are met, the system generates the electronic invoice according to Annex No. 3, which includes: the 5% tax amount, the service fee, and the payment reference.

The invoice is delivered to the applicant through e-Albania. If the process were done physically at the counter, the invoice would be printed and handed there. The payment deadline is indicated on the invoice and is 30 days from the generation date.

If the application is rejected by ASHK, the individual is notified electronically with the reason and may correct and reapply.

Step 3: Payment of the tax and fee

After receiving the invoice, you pay at any second-tier bank, entering the invoice reference. Individuals pay into the special account of the local ASHK directorate. This system is important to understand: ASHK functions as a tax agent, collects the amount, and by the 10th of each following month transfers the tax collected during the previous month to the state budget account under code 7020900.

This implies something practical: if you pay the revaluation tax on 28 December 2026, ASHK transfers it to the budget by 10 January 2027. The 31 December 2026 deadline refers to the payment date, not the transfer date.

Step 4: Entry in the cadastral register within 5 working days

Within 5 working days from payment verification, ASHK makes the entries on the cadastral card. In section “A” it records: the revaluation date (= the tax payment date), the new value, and the archival reference of the document.

This 5-day deadline is mandatory and legally clear. If ASHK does not act within it, you have a legal basis to submit a written request.

Step 5: Obtaining the updated cadastral card

After registration, you may request a copy of the cadastral card with the new value—by paying the standard cadastral fee. This new certificate is your new base document—keep it as your new cost base for any future transaction involving the property.

If you plan to apply in November or December 2026, be aware that a high volume of applications at ASHK offices may slow down verification and invoice generation. Since the deadline depends on the payment date and not the application date, any delay by ASHK risks pushing you past the deadline. We recommend applying during March–October 2026.

Official service fees — the table and the RVP code

Instruction 5/2026 (Chapter VIII) publishes for the first time the official cadastral service fee that ASHK applies to the revaluation process. The service code per the table is RVP, and the fee varies according to the size of the 5% tax paid, not the absolute value of the property.

When the 5% revaluation tax is up to 150,000 ALL, the RVP service fee is 3,500 ALL.

When the 5% revaluation tax is from 150,001 to 300,000 ALL, the RVP service fee is 7,000 ALL.

When the 5% revaluation tax is over 300,001 ALL, the RVP service fee is 10,000 ALL.

The service fee is paid separately from the 5% tax, and together they form the total administrative cost. If you have chosen a private expert, the cost of the expert’s report is added—currently ranging in the market between 30,000 and 100,000 ALL per property, depending on type and area.

Total cost example: property with a revaluation difference of 10,000,000 ALL. 5% tax: 500,000 ALL. RVP fee: 10,000 ALL. If you add expert cost, e.g., 60,000 ALL, total process cost: 570,000 ALL. Compared with the sale tax without revaluation: if you sold tomorrow for 13,000,000 ALL, the 15% tax would be around 1,500,000 ALL (if the previous value was low). Net savings: around 930,000 ALL.

Does the property have to be registered? — three possible scenarios

The question “must the property be registered before revaluation” has come up often and is legitimate, because Albania still has thousands of properties with unclear cadastral status. Instruction 5/2026 (Chapter V) addresses it precisely through three scenarios.

Scenario 1 — fully registered property, appearing on the cadastral card

This is the standard case. If your property has a complete cadastral card and appears as active, the revaluation process proceeds without obstacles. The revaluation entries are reflected directly in section “A” of the existing card. No preliminary step is needed.

Scenario 2 — property is in a registered area but does not appear in the cadastral register

This often happens with properties that have an ownership title (certificate, AMTP, court decision, inheritance certificate) but were never registered in the cadastral system. Typical cases: inherited property where the inheritance certificate was never submitted to ASHK, purchased property where the notarial deed was not presented for registration, or post-2000 new construction without a final certificate.

The law is clear: first you must apply for registration of the property through e-Albania, submitting the ownership title and supporting documentation. Only after the property is registered can you apply for revaluation. This additional step takes time—plan ahead if you are in this situation.

Scenario 3 — property is in a cadastral zone without initial registration

This is the most delicate case and requires special attention. There are rural and peripheral zones where the state’s initial cadastral registration process (the first inventory of all properties in the zone) has not yet begun or has not been completed. In these zones, properties do not have a classic cadastral card.

The Instruction provides that revaluation can also proceed for these properties—entries are recorded in the mortgage register or provisional cards. After completion of the zone’s initial registration, if your title is confirmed as lawful, the revaluation entries are transferred to the regular cadastral card.

But beware: if your title is rejected during the initial registration process, the revaluation value is not reflected and the tax paid is not refunded. Therefore, before paying the revaluation tax for a property in a zone without initial registration, consult a legal expert about the status and legal strength of your ownership document. The risk is not zero.

What changes for legal entities — procedure, documents, and accounting effects

Businesses—commercial companies (SHAs, LLCs) and any other legal entity—have the right and opportunity to revalue, but their procedure differs fundamentally from that of individuals. Instruction 5/2026 (Chapter VI) addresses them in detail.

Where are the documents submitted?

Businesses do not apply to ASHK. The application and documentation are submitted to the Regional Tax Directorate (DRT) where the legal entity is registered for tax purposes. This is the first and fundamental procedural difference.

Who performs the valuation?

Businesses do not have the option of ASHK valuation using fiscal prices. The only lawful method for legal entities is valuation by an independent licensed expert. This means additional cost for the expert’s fee, but also a real market value—which, as explained, is tax-advantageous if you plan to sell.

What serves as the tax base?

Unlike individuals, where the deductible value is the historical purchase price, for businesses the deductible value is the book value of the asset per the 2025 financial statements—i.e., purchase price minus accumulated accounting depreciation up to 31 December 2025. Therefore, the more depreciated the property is, the higher the revaluation tax base and the higher the 5% tax. But at the same time, the greater the savings on sale tax.

Revaluation difference and accounting effects

After revaluation and registration, the difference between the revaluation value and the previous book value is recorded as an increase in the asset’s value in the balance sheet (debit tangible fixed assets), with the corresponding credit either to a revaluation reserve under equity (credit additional capital) or to a reduction of retained losses. Effect: the company’s balance sheet strengthens, the debt-to-equity ratio improves, and the property can serve as collateral at a much higher value with banks.

Required documents to submit to the DRT

— Voluntary declaration for revaluation in accordance with Annex No. 2 of Instruction 5/2026.

— Power of attorney of the legal representative, if the procedure is carried out by someone other than the administrator.

— Copy of the license and identification of the independent expert.

— Copy of the invoice for the private expert’s service.

— The original valuation report — it must be the signed and stamped original, not a photocopy.

— The 2025 financial statements (balance sheet + profit and loss statement), where the revalued property appears as tangible fixed assets, together with the explanatory notes.

— Copy of the payment mandate for the 5% tax, made in accordance with the template in Annex No. 4 using code 7020400.

The revaluation date for legal entities, as for individuals, is considered the date the tax payment is made.

Depreciation of the revaluation is not recognized for tax purposes

This section addresses business clients directly and is where misunderstandings are most frequent.

After revaluation, the asset’s value increases significantly in the balance sheet. Logically, many accountants and managers think: “Since the asset value increased by 40,000,000 ALL, we can now depreciate that increase as a tax-deductible expense.” This is incorrect and the law is clear.

Article 2, point 5 of Law 85/2025 and Instruction 5/2026 (Chapter VI, point 2.2) explicitly specify: the difference between the revaluation value and the previous book value is not subject to depreciation for tax purposes.

In practice: the company records the new asset value in the balance sheet (positive accounting effect—higher assets, higher equity), but cannot depreciate the value increase as a deductible tax expense year by year. Only the original historical purchase cost continues to be depreciated under existing rates and schedules.

Full example:

Company “Beta LLC” bought a business building in 2013 for 45,000,000 ALL. After 13 years of depreciation at 5% annually, today’s book value is: 45,000,000 − (45,000,000 × 5% × 13) = 15,750,000 ALL. The expert values the building today at 95,000,000 ALL.

Revaluation difference: 95,000,000 − 15,750,000 = 79,250,000 ALL.

5% revaluation tax: 79,250,000 × 5% = 3,962,500 ALL.

5% tax as a deductible expense against corporate income tax (15% × 3,962,500): −594,375 ALL corporate income tax saving.

Net revaluation cost: 3,962,500 − 594,375 = 3,368,125 ALL.

Additional tax depreciation from the 79,250,000 ALL difference: zero — not allowed.If the property is sold after 2 years for 105,000,000 ALL:

Without revaluation — capital gain: 105,000,000 − 15,750,000 = 89,250,000 → 15% tax: 13,387,500 ALL.

With revaluation — capital gain: 105,000,000 − 95,000,000 = 10,000,000 → 15% tax: 1,500,000 ALL.

Sale tax savings: 11,887,500 ALL.

Net revaluation cost: 3,368,125 ALL.

Net tax benefit: 11,887,500 − 3,368,125 = 8,519,375 ALL.This large difference—around 8.5 million ALL in net savings—clearly justifies revaluation for businesses planning a short- or medium-term sale. Even if you do not plan to sell, the fact that the property can serve as collateral at 95,000,000 ALL (instead of 15,750,000 ALL book value) may open access to much larger bank financing.

If you have paid incorrectly — how the tax is refunded according to the instruction

Instruction 5/2026 (Chapter VII) explicitly regulates the refund procedure for tax paid in error. This mechanism was missing as an explicit instruction and is now clear.

If you determine that the payment was wrong—too much, wrong property, duplicate application—the procedure depends on when you identify the error.

If you submit the request by the 10th of the following month after the payment date, the local ASHK directorate has the authority to refund the amount directly. No other step is required—submit a written request, attach the original payment mandate and evidence of the error, and ASHK processes it.

If the 10-day deadline has passed and the amount has already been transferred to the state budget account, the route is different. Submit your request to the competent Tax Directorate (not ASHK). The Tax Directorate requests from the local ASHK directorate the supporting documentation confirming the error. After administering it, it processes the refund to the individual or business.

Practical advice: if after payment you notice any anomaly or doubt, act within the week—not within the month. The sooner you respond, the simpler the procedure.

Frequently asked questions after the instruction’s issuance

After the instruction was issued, we received concrete questions from clients and readers. Here are the answers directly based on the text of the instruction.

Can I revalue a property if I bought it after 2020 and the value hasn’t changed much?

Yes, you can. There is no restriction based on the purchase year. However, if today’s market value is similar to the purchase price, the tax base will be small and the 5% tax will not be high, but future savings will not be significant either. Revaluation makes sense when there is a significant difference between the existing value and the current market value.

Can I revalue a property if I already revalued during 2020–2022?

Yes, absolutely. Instruction 5/2026 (Chapter I, point 1) explicitly specifies: “This includes cases where revaluation of the immovable property has also been done previously, in implementation of previous revaluation laws.” In this case, the deductible value will be the 2020–2022 revaluation value, if that was the last value on which you paid tax.

Can I revalue only one of several properties?

Yes. Revaluation is individual and voluntary for each property. There is no obligation to revalue all properties at once. Analyze each property separately—calculate the difference, the 5% tax, the process cost, and the outlook for sale or transfer, then decide for each.

If I sell the property during 2026 without revaluing, can I revalue before the sale deed?

In theory, yes—revaluation and sale are separate legal acts. But the revaluation must be completed and registered (within 5 working days after payment) before signing the notarial sale deed. The notary will check the cadastral card and calculate the tax based on the last registered value. If the revaluation is not yet reflected on the card, the notary will apply the previous value. Therefore, timing matters.

If the property has co-owners, what happens?

Each co-owner can revalue their share separately, without needing agreement from the others. ASHK verifies each applicant’s ownership and processes their share. However, practically, if other co-owners do not revalue, they will pay 15% capital gains tax on their share when selling—while the one who revalued will pay much less.

Our business has properties with zero book value (fully depreciated). Is revaluation worth it?

Very often yes. When book value is zero or near zero, the revaluation tax base (= expert value − 0) is high, meaning a high 5% tax. But the 15% sale tax savings, calculated on the same absolute value, will be three times the 5% tax paid. Therefore, the math usually comes out positive, especially if you plan to sell.

Where can I find the reference price for my zone?

Reference prices for buildings are based on Council of Ministers Decision No. 132/2018 “On approving reference prices for categories of immovable property” and its revisions. The value map for land is based on the applicable secondary legislation. These data are administered by ASHK and applied automatically during calculation. You may request preliminary information at ASHK counters or through a licensed expert before applying.

Conclusion

Instruction No. 5/2026 did not change the law—the law is the one adopted in December 2025. What it brought was the real possibility of implementation. Now the procedure exists, the forms exist, the fees are known, and ASHK has clear time-bound obligations. The phase of waiting and uncertainty is over.

The 31 December 2026 deadline may seem far away, but if you consider the process time (2 working days for the invoice + 5 working days for registration) and the possibility of a high volume of applications in the final months, we recommend applying during March–October 2026. The risk of postponing the application to December is real, and tax paid after 31 December 2026 will not be recognized under the current law.

Revaluation is not merely a bureaucratic procedure—it is a financial decision. Before deciding, calculate the difference, the 5% tax, the expert cost if needed, and the real outlook for your property. Only with concrete calculations can you decide with confidence.