Decision No. 132, dated March 7, 2018 On the methodology for determining the taxable value of real estate “building,” and the tax base for specific categories, the nature and priority of information and data for determining the tax base, as well as the criteria and rules for the alternative assessment of the tax liability.

Decision

In support of Article 100 of the Constitution and Articles 21, 22/1, 22/3, and 22/4 of Law No. 9632, dated 30.10.2006, “On the System of Local Taxes,” as amended, on the proposal of the Minister of Finance and Economy, the Council of Ministers

SET:

Article 1

Definitions

For the purpose of applying the methodology for determining the taxable base of real estate “building,” the following terms shall have the meanings set forth below:

1. “Appraised price,” the unit of measurement of value per square meter of the real estate property's building area. This price may be the market price or the estimated price determined by this methodology.

2. “Zonal division/subdivision,” a territorial area within the local self-government unit with a unique cadastral name and number. These divisions/subdivisions are represented as land parcels with defined boundaries that separate them from one another.

3. “Building,” the object(s) constructed on or under the surface of the land or attached to the land and constituting a building structure with one or more ownership units, which is subject to the building tax as defined by law.

4. “Unfinished building” means the building as a whole or any part of an existing structure for which the developer has obtained a building permit but has failed to complete it within the deadline specified in the approval document for the building permit application.

5. “Property unit,” a building or part thereof that is owned or used by an individual, a natural person, or a legal person, and that is legally separated from other real estate properties of the “building.” The ownership unit may be used for residential purposes and/or for economic activity, etc.

6. “Residential ownership unit subdivision,” the portion of the ownership unit used for residential purposes.

7. “Division of the ownership unit for economic activity,” the part of the ownership unit used for the purpose of economic activity.

8. “User” means the individual, natural person or legal entity, who uses the building/property unit for residential purposes, economic activity or non-economic activity, regardless of whether that building/property unit has a title of ownership or not.

9. “Central register of the real estate database” (Tax Cadastre), the central database system, which serves for the entry, processing, and correction of data related to real estate, which serve for the purpose of calculating the amount of real estate tax to be paid by each taxpayer. This register provides information to users.

10. “Taxpayer” means any individual, natural or legal person, domestic or foreign, owner or user of real estate in the territory of the Republic of Albania, regardless of the level of use of such buildings. The obligation to pay the tax on the real estate “building” rests, as the case may be, with the owner or co-owner, according to the share they hold, or the user of the real estate, for properties that are not equipped with ownership documents, the persons who have applied for the legalization of the building, developers who fail to complete construction in accordance with the relevant permit issued by the local self-government unit.

11. “Property value,” the current value of the real property building/unit ownership as documented in legal records or the value determined by one of the methods described in this methodology. Property value is the taxable base on which the real estate tax rate for a building/property unit is applied. Property value is calculated by multiplying the price per square meter by the area of the building/property unit.

12. “Economic activity” means any activity carried out by producers, traders, or persons supplying goods and services, including extractive, industrial, commercial, service, agricultural, and professional activities. Economic activity is also considered to include the exploitation of embodied or intangible assets with the aim of generating ongoing income.

Neni 2

Methodology for determining the taxable value of real estate “building”

1. Determination of the assessed price and the area of the building/property unit

The determination of the taxable value of real estate—a building or ownership unit—is based on valuation priorities, following a specific order. The assessment basis relies on self-declaration as an obligation for every taxpayer, and alternative methods are applied if the self-declaration is not made, is inaccurate, or if complete data for a fair assessment of the building/real estate property are not available.property unit, which must be taxed.

Local self-government units, for the purpose of determining the taxable base of a building as real estate, follow this order of valuation:

1.1 Self-declaration

Every taxpayer must self-declare the data for his real estate—building(s) or ownership unit(s)—that he owns or uses.

Self-declaration is made at the local self-government unit or any institution authorized by the government or local self-government units, to obtain and process the taxpayer's self-declared information for the purpose of enforcing the relevant real estate tax legislation.

If the taxpayer's self-declared value differs from the value calculated using the estimated price determined by this methodology, the higher value will be taken as the tax base.

In the initial phase of implementing the law No. 9632, dated October 30, 2006, For the “Local Tax System,” as amended, data provided by government-authorized institutions or local self-government units, which serve to assess real estate and determine the tax base, may be considered and used.

1.2 Determination of the assessed value and the building's area, based on the real estate registry maintained by the local land registry offices (ZVRPP)

For determining the tax base for the building/property unit, the value determined by the revaluation of the property registered with the ZVRPPs will serve as the reference.

If the information obtained from the Land Registry shows that a sale transaction for the building/property unit has taken place within the last three years, then the higher of the transaction price and the value registered in the Land Registry will be taken as the taxable basis.

1.3 Determination of the estimated price based on average sale and purchase prices of buildings/property units

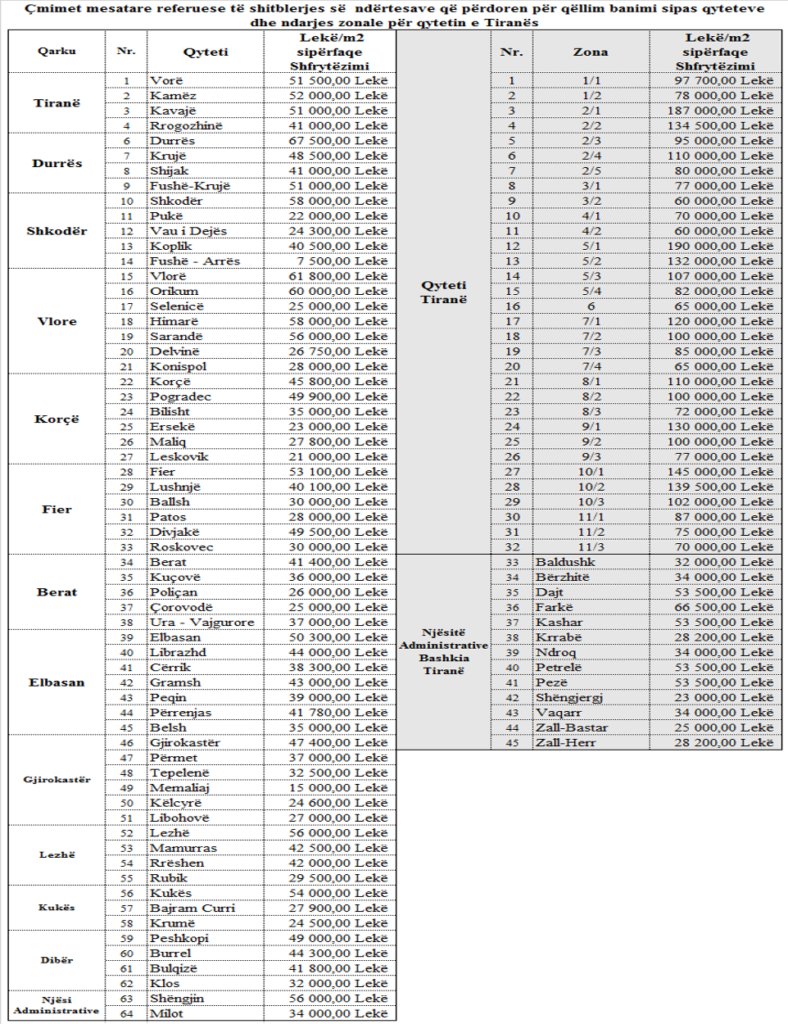

When the assessment under points 1.1 and 1.2 above is impossible, the estimated price for the valuation of the real estate property building/property unit will correspond to the average reference price of buildings used for residential purposes by city, as specified in Annex 1 attached hereto and forming an integral part of this decision.

For subcategories of non-residential buildings, based on their intended use, the average prices per square meter of building area, as specified in Annex 2 attached to this decision and forming an integral part thereof, shall apply.

If the price per square meter for a dwelling/unit of ownership provided by the ZVRPP and the minimum fiscal prices differ, then the higher of the two is taken as the valuation price.

2. The value of the real estate asset “building,” based on field verifications.

Local self-government units, in accordance with the powers of the applicable legal framework, make corrections to the database registry. The corrections are carried out based on periodic on-site verifications of the building's/property unit's area.

The field verification also serves to record for the first time the building/property unit or its subdivision. In this case, the local self-government units request information from official sources, if available, on the area of the building/property unit or its subdivision and compare it with the verification conducted. If they do not obtain information regarding the area of the identified buildings, the local self-government units carry out their own assessment of the building/property unit based on the area verified on-site.

Local self-government units, according to the procedures specified in this methodology, In any case, after assessing the value of the real estate, they enter the data into the database register for the purpose of determining the tax base and calculating the amount of tax to be paid by the taxpayer.

2.1 Presumed surface

If existence is identified but the building's/unit's floor area cannot be determined, the following reference values for area shall be used:

a) 100 (one hundred) square meters of floor area per property unit for residential buildings;

b) 70 (seventy) square meters of area per ownership unit for residential buildings privatized under the law. No. 7652, dated December 23, 1992, “On the Privatization of State-Owned Housing,” as amended.

For other buildings not used for residential purposes, local self-government units conduct on-site verification to determine the area and calculate the tax base.

When, during field inspections, damage to buildings is found due to natural disasters (earthquake/fire/flood, etc.), which alter the value of this property, the local self-government unit, depending on the case presented to it, establishes a commission that assesses and adjusts the building's value. The assessment is made based on the physical condition in which the damaged building is found.

3. Zonal/subzonal subdivision within the territory of the local self-government unit

Units of local self-government may adopt zoning/subzoning subdivisions of the territory within their jurisdiction for the implementation of tax rate levels within plus or minus 30 (thirty) percent of the boundaries.

The council of the local self-government unit, no more frequently than once a year, for dwellings in the administrative units outside the respective city that joined the local government units after the entry into force of Law No. 115/2014, may reduce the average reference price set out in Annex 1 by up to minus 35 (thirty-five) percent compared with the price of the nearest zone, excluding residential areas. In areas within the Municipality of Tirana, this reduction is up to 30 (thirty) percent compared to the price of the nearest area, excluding residential zones.

The approved levels for the zones/subzones of the local self-government unit's territory are officially notified to the General Directorate of Property Tax.

4. Value of real estate for unfinished buildings in violation of the building permit deadline

For buildings that have a building permit but have not been completed by the deadline specified in the approval document, the taxable base is determined based on the estimated construction cost, based on the building permit approved by the relevant local self-government unit or the Municipal Tax Authority (KKT). In this case, the value of the building's tax base is calculated for the entire building when it is a single unit and intended for a single purpose of use, regardless of the stage at which the unfinished building is. The building tax base is calculated at 30 (thirty) percent of the tax rate established by law, multiplied by the construction cost specified in the approved building permit.

In the event that the building consists of more than one property unit, intended for different purposes or to be owned by more than one owner/the user, the full cost of constructing all the building's constituent units shall serve as the tax base, regardless of the phase at which the entire unfinished building is. If the building's units, based on the approved construction permit, are intended for different uses (for example, some for residential purposes and some for economic activities/non-economic), the real estate value for determining the building tax base is calculated at 30 (thirty) percent of the tax rate set by law, according to the type of use, multiplied by the construction cost per unit of the building.

If the developers have entered into a sales contract for the transfer of ownership of the unfinished building or of its individual units, the sales contracts shall serve as the basis for the valuation of the real estate for the purpose of calculating the building tax. If the comparison shows that the value of the sales contracts differs from the value calculated using the assessed price, then the higher value is determined as the tax base.

When a field verification shows that the building or certain units thereof have been put into use/exploitation, regardless of whether the building as a whole is complete, the tax is calculated in full on the portion that is in use/exploitation. In this case, the taxable base is calculated using construction costs for the unfinished portion and appraised values for the parts placed into use. For parts of the building placed into use, the tax base will be full. The same situation applies when the building use permit has not been issued or the registration with the local real estate registry office has not been completed.

In all cases referred to in paragraph 4 of this article, the person liable for payment of the calculated tax is the developer. In cases where individual units of the building have been put into use and the tax is paid in full, the payer of the calculated tax is the user.

5. Calculation of the building/unit ownership tax amount

Local self-government units, using the data collected on the building/property unit, determine the tax base and calculate the annual building tax amount to be paid by each taxpayer. The basis for calculating the building tax is the value of the building/property unit, determined by one of the methods provided in this methodology.

For the purpose of calculating the tax on the building/property unit, the tax base is multiplied by the statutory percentage tax rate, as follows:

a) 0.051 TP3T, for the building/owner-occupied unit used for residential purposes;

b) 0.21 TP3T, for the building/property unit that is used, exploited for economic activities;

c) 30% of the respective tax rate on the entire building area for which the developer has been issued a building permit and has failed to complete it within the deadline specified in the approval document for the building permit application.

6. Procedure for collecting information from field verification

6.1 On-site verification for the appraisal of real estate is carried out, in any case, by order of the head of the relevant local self-government unit in whose territory the building/property unit to be appraised is located. The verification order contains:

a) the identifying data for the building/property unit (address, administrative unit, location, owner/user, etc.) and the taxpayer (name of the individual, natural person, legal entity);

b) the purpose of carrying out the assessment process of the building/property unit;

c) the time when the verification will be carried out and the possible deadline for the verification process;

c) the name(s) of the employees of the local self-government unit who will carry out the verification;

d) the date and time when the employees of the local self-government unit will appear to carry out the verification.

If the verification process requires the completion of the relevant forms, these forms are sent in advance to the taxable person, together with a copy of the verification order.

The order notifying the completion of the verification process is sent by mail or hand delivery, with the signature of the taxable person who has received it. In the case of postal delivery, the order is deemed received ten (10) days after it was delivered to the post office.

6.2 In advance, in the notification of the audit's conduct, the taxpayer must be informed of the object of the on-site audit procedure, the reasons for which this audit is required to be conducted, the taxpayer's rights to express opinions, remarks, or objections regarding the verification process conducted by the employees of the local self-government unit at the conclusion of that process, as well as to be informed that, in the event this process is not carried out, the local self-government unit has the right to carry out the assessment using alternative methods and to determine the amount of the annual tax to be paid based on this assessment.

6.3 In the event that the taxable person is not found at the scheduled date and time for the verification process, the local self-government unit issues a second notice and, if the same situation recurs, the employees of the local self-government unit carry out the assessment using the alternative methods specified in this methodology.

6.4 In the case of on-site verification, the employees of the local self-government unit are required to draw up the verification report and to record the date on which the verification process was completed, their first name, last name, and signature at the end of the report they have prepared.

6.5 Employees of the local self-government unit are required to inform the taxpayer of the verification result by clearly reading aloud, in his presence, the contents of the written material in the verification record and, at the conclusion, to also request the taxpayer's counter-signature for the contents of the verification act. The taxpayer has the right to make their own corresponding notes, if they wish, regarding the content of the verification act, any remarks or objections they have. Additionally, the taxpayer, in addition to their name, surname, and signature, also enters the date on which they made their signature.

6.6 When the taxpayer prevents the employees of the local self-government unit from carrying out their duties, as ordered by the local self-government unit for this purpose, the full tax will be assessed against them. In this case, the areas will be assessed using alternative valuation methods, as specified in this methodology.

6.7 In cases where the field verification reveals buildings/property units for which there is no complete or partial prior information, the local self-government unit employee, by means of a minutes, takes measures to complete the identifying data as follows:

a) Address, geographic location coordinates, the area of the building/property unit;

b) The purpose of using the building/property unit;

c) The identifying information provided for the taxpayer;

c) The name(s) of the employees of the local self-government unit who carried out the verification;

d) The date and time when the employees of the local self-government unit carried out the verification;

dh) Any other information necessary to identify the building/property unit, the taxpayer, and to determine the taxable base.

In this case, the taxpayer must be notified of the calculated tax liability.

6.8 The deadline for entering the data obtained from the field verification into the real estate database system must not be later than 30 calendar days from the date of the verification act.

In any case of a change to the data in the database system, whether from field verification, as a result of correction or a decision by the local appeals body, or after a final decision issued by the Administrative Court, the data entry must not be later than 30 (thirty) calendar days from the date the decision is received.

6.9 Data loading into the database system must not impair the system's functionality. The General Directorate of Property Tax, if it determines that data loading could harm the system, will intervene and carry out the data loading into the system.

7. Periodic on-site verification of the real estate asset “building”

The local self-government unit has the right to conduct field verifications each year covering up to 20 (twenty) percent of its territory. In this case, the verification process serves to verify possible changes in existing buildings/property units that affect changes in the value of real estate and, consequently, the amount of tax to be paid. Such changes relate to an increase in the building's floor area/the property unit, additions in floors, structural improvements, property alienation, change of use, and which requires changing the tax rate, tax exemption, or the loss of the right to tax exemption, etc. This process also serves to identify new buildings/property units not yet entered into the system.

In the event of verifying buildings/property units that do not appear in the central data system, the local self-government unit must carry out their full registration by completing all information elements required by the system.

In all of the above cases, the local self-government unit must notify the taxpayer of the obligation that has arisen.

8. Verification of data by the municipal official responsible for the real property tax on buildings.

The officer responsible for the building tax at the local self-government unit has the right and obligation to review and verify all documentation collected during the field verification process, the verification report prepared, and to confirm their accuracy.

If the documentation contains errors, omissions, or inaccuracies, it requests that the employees who completed the documentation review it and, if necessary, repeat the verification procedure.

9. Correction of data related to tax calculation in cases of clarifying information on area, zoning location, and corresponding prices.

The taxpayer, at any time, when he believes that the assessment of his real property—the taxable object—is inaccurate, has the right to request a correction of the tax liability.

The taxpayer, upon receiving the property tax assessment notice, if they do not agree with this valuation, has the right to request a correction of the value:

a) at the local tax office of the respective local self-government unit, in the territory where the real estate property “building” is located, accompanied by the supporting documentation; or

b) at the tax collection agent's office, in cases where the correction service is provided by the local self-government unit with its own employees.

The right, if any, to correct the final value of the real estate asset “building” will be determined after the authorized body within the local self-government unit reviews the appeal and issues a final decision.

The local tax office, within 30 (thirty) days, reviews the taxpayer's request regarding whether or not it will be taken into consideration, makes corrections if the initial assessment contained errors, and provides the taxpayer with a written response.

10. Administrative Appeal and Judicial Appeal

If, even after receiving the response regarding the right of correction, the taxpayer does not agree with the position of the tax office at the local self-government unit, he has the right, based on Article 7, “Appeal,” of Law No. 9632, dated 30.10.2006, “On the Local Tax System,” as amended, to address the local tax appeals body established for this purpose within the local self-government unit. The local tax appeals body issues its decision within the legal deadline provided for in the tax legislation.

If the taxpayer still disagrees with the decision issued by the local tax appeals body, they appeal to the Administrative Court. The decision of the Administrative Court is considered final and will serve to correct the taxable base value and, consequently, the amount of tax payable by the taxpayer.

The emergence of the obligation to pay the property tax on a building/unit of ownership after the detection of changes from on-site verification.

In cases where field verifications result in a change in the tax base value, the calculated tax amount is reflected as the tax payable as of the date the change is recorded in the field by the relevant verification report. In any case, the verification report must be signed by the taxpayer to whom this change was noted during the conducted verification.

12. Change in the building's use from what is recorded in the database system.

If units of local self-government determine changes in the use of real estate—a building/property unit or part of a property unit—which consequently lead to a change in the tax base value, accordingly, and the amount of tax to be paid by the taxpayer, the tax due for the remainder of the year after the change is determined is adjusted, and the tax is collected for the actual corrected amount.

Changes to the obligation to pay take effect as of the date of the determination recorded in the verification act.

In any case, the verification form must be signed by the taxpayer to whom this change was noted during the verification.

Article 3

Specific building subcategories and intended use

The subcategorization of nonresidential buildings/property units by their intended use and exploitation is specified in Annex 2 attached to this decision.

The subcategories of buildings/property units used for residential/housing purposes are as follows:

1. A building that serves people's basic housing needs, including houses, apartments, dwellings, and similar structures.;

2. Closed garages;

3. Basements;

4. Any other similar building, above or below ground, that is not used or exploited for any purpose other than residential.

Article 4

The nature of the information and data used to determine the tax base on buildings and to inform the public.

1. Sources of information (primary data)

Possible sources of information, for the purposes of administering the property tax on buildings, are:

a) The taxpayer's self-declared data on the building/building unit owned or used by him;

b) Data available from the ZVRPPs regarding the assessment and reassessment of buildings, as well as the property titles over them;

c) Data from the urban planning offices on building permits issued;

c) Data from notary offices on transactions for the sale and purchase of buildings;

d) ALUIZNI data for buildings in the legalization process;

dh) Data secured through field verification by the local self-government units themselves;

e) Data from the Central Civil Registry;

e) Data from economic operators that have contact with consumers, such as the Electricity Distribution Operator, water and sewerage companies, or other institutions not mentioned above, which hold information on the building asset/building unit, property titles or the legal status of the taxpayer's relationship with the real estate asset, the subject of taxation, as well as regarding the taxpayer himself;

f) Data from the Property Treatment Agency on properties treated under KKKP decisions.

2. Information on primary data must include:

2.1 Identifying data for the real estate property – building/unit ownership;

2.2 The destination or destinations of use of the building/property unit or of its separate units;

2.3 Identifying information for the taxpayer;

2.4 Data on the taxpayer's legal status regarding the taxable property and his share to be taxed.

3. Primary data on buildings for identification and assessment purposes.

The data for the buildings include:

3.1 The unit of local self-government and the administrative unit in the territory over which the building/property unit is located;

3.2 The cadastral zone in which the building is located, as defined by the relevant sectoral legislation.;

3.3 The exact address of the building/unit of ownership, including the street name, building number (entrance and apartment number, when the building is a co-owned unit), as well as other information identifying the precise location of the building/unit of ownership;

3.4 Type of building:

a) A separate building;

b) A co-owned building (consisting of ownership units, each with its own owner);

3.5 Building restrictions on all of its sides;

3.6 The number of stories in the building, which includes:

a) The total number of floors above the ground surface;

b) The total number of floors below the ground surface;

3.7 Year of construction and the built-up area;

3.8 Other identifying elements.

4. The central system for calculating the taxable base value of real estate must contain data for each property unit, as follows:

4.1 The unique identifying number of the real estate property;

4.2 The entrance number, the apartment number, the number of the building's separate unit/unit ownership, and which is attached to the street name and entrance number;

4.3 The floor on which the unit property is located;

4.4 Area in square meters, which indicates the surface area intended or used for a specific purpose, expressed in total square meters. The measurement of the property unit's area is carried out in accordance with the criteria specified for this purpose in the relevant legislation.

4.5 Basements and sub-attics of buildings/owner-occupied units that, upon on-site verification, are found to be intended for or used for:

a) storage of household items, without any profit motive, is recorded with the comment “basement/attic (as applicable) for storing household items”;

b) for residential purposes, they are recorded with the comment “for residential purposes”;

c) for profit purposes, are recorded with the comment “for profit purposes.”.

In the cases of letters “a,” “b,” and “c” above, the calculation of the value of the property unit is made separately when the part of the building is treated as a separate, distinct unit of the building, even if it is not owned by an identified person, but is in use and used by him for one of these purposes. When this property unit is in common use by several owners/by several owners/users of other property units in the same building, the calculated total of the tax base value, as well as the taxable portion of the calculated tax, is apportioned equally among all its users.

4.6 Year of construction;

4.7 The cadastral area of assessment;

4.8 Assessment category based on minimum tax rates (assessor);

4.9 Destination of use:

a) Housing;

b) Trade, services;

c) Production, processing, storage, keeping, or breeding of live animals;

c) Abandoned;

d) Incomplete;

dh) Other, not specified in the classifications above.

4.10 GPS coordinates.

5. The central system for calculating the taxable base value of real estate must contain the taxpayer's data as follows:

5.1 The personal identification number of the owner/user of the real estate property (the taxpayer);

5.2 The name, father's name, and surname of the taxpayer, owner/user of the real estate;

5.3 NIPT/NUIS (for individuals, natural persons, or legal entities engaged in economic activity in real estate, the taxable object);

5.4 The name registered with the National Business Center (NBC) for the economic activity;

5.5 The name of the taxable entity's legal representative;

5.6 The address of the real property—the building, the taxable object;

5.7 The name of the local self-government unit (municipality), as well as of the administrative unit in whose territory the real estate property—the building, the taxable object—is located;

5.8 Any other identifying information that completes the accurate identification of the taxable person and the location of the real estate property, the object of taxation.

6. Central system for calculating the taxable base value of real estate

The act establishing the central system for calculating taxes on real estate is enacted by a special decision of the Council of Ministers.

7. Public Information

7.1. Units of local self-government must continuously inform taxpayers within their territory about the procedures and criteria for calculating the tax, taxpayers' rights to correction and appeal, the method of payment, and the measures applied in case of non-payment of the tax.

7.2 Public information serves the transparency of local self-government units, but, at the same time, it also serves to enable the acquisition of information for the purpose of facilitating the real estate assessment process and the objectivity of the assessed value, through information that taxpayers themselves must provide to local self-government units regarding the real estate they own or use.

7.3 Public information is provided through electronic information channels, the media, public notices, and any other form of communication with the public that may be used for this purpose.

7.4 Notices are intended to inform the public about:

a) the registration of new real estate objects: building/unit ownership;

b) real estate objects—buildings/ownership units—that have undergone changes in use or purpose;

c) real property—a dilapidated, abandoned, or uninhabitable building or ownership unit;

c) the results from verifications carried out in the field.

d) decisions made by the local self-government unit regarding the real estate property tax, the levels set for the tax amount to be paid according to zonal or sub-zonal divisions, etc.

Article 5

The institutions and bodies entrusted with the task for implementation

The ministry responsible for finance, the General Directorate of the Wealth Tax, and the units of local self-government are charged with implementing this decision.

This decision enters into force upon publication in the Official Gazette and takes effect on April 1, 2018.

***

Annex 1

Average reference prices for the sale and purchase of residential buildings by city and zoning classification for the city of Tirana.

Cadastral areas

ZONE 1

1/1 Ali Demi Cinema, Sports Field, Shkozë Village, Water Depot; 1/2 Polygraphic, Shkozë, Tractors, Shkozë Village, LanaBregas, Linzë, Sauk

ZONE 2

2/1 The Pyramid, Qemal Stafa Stadium; 2/2 New Bazaar, the 9-story buildings, Avni Rustemi School; 2/3 Ministry of Foreign Affairs, Ambulance No. 1, Bërryli; 2/4 Ballet School, U.S. Embassy; 2/5 Student City, Faculty of Economics, Martyrs“ Cemetery, Sauk, Selitë

ZONE 3

3/1) Xhamllëku, Profarma, Bardhyl Street, Congress of Manastir Street, Jeanne d'Arc Boulevard; 3/2) Porcelan, IK V, Film Studio, Hoxha Tahsim Street, Old Lana, Linzë village.

ZONE 4

4/1 Hospital Complex, SHIK, Oxhaku, New Allias, Tufinë village; 4/2 Allias, “Njazi Meka” Street, Riverbank, New Allias, “Myslym Keta” and “5 May” Streets”

ZONE 5

5/1 Former Block, University Bookstore, Vodafone; 5/2 “Selman Stermasi” Stadium, Shushica, Artificial Lake; 5/3 Botanical Garden, “Komuna e Parisit” Street, Artificial Lake; 5/4 Hotel “Diplomat,” “Vasil Shanto” Block, Small Selite.

Zona 6: Technological School, Kombinati, Vaqar, Selitë, Yzberisht, Sharrë

ZONE 7

7/1 Court of the District, Former “Albania Today” Exhibition; 7/2 Embassy Block, Faculty of Civil Engineering; 7/3 NSHRAK, Ministry of the Interior park, Bread Factory; 7/4 New Ring Road, Flour Mill, former Aviation Field, Yzberisht

ZONE 8

8/1 Selvia, “Partizani” High School, Tafajt Street; 8/2 Medreseja, Pharmacy No. 10, Industrial Market; 8/3 Industrial Market, “Ajka” Factory, “Dinamo” Plant, Riverbank.

ZONA 9

9/1 Bar Piazza, the block along “Zogu I,” Barrikadave Street, Fortuzi Street, Sulejman Pasha Street to Mine Peza; 9/2 Train Station, General Archives, Land Registry, Polytechnic; 9/3 “Don Bosco,” Shoe Factory, Riverbank, Polytechnic, Siri Kodra Street“

ZONE 10

10/1 PTT, the Telecom, former Writers“ Union; 10/2 Myslym Shyri Street, Police Directorate, Catholic Church; 10/3 Embassy Block, Prosecutor's Office, Durrës Street.

ZONE 11

11/1 Black Bird, former Party School; 11/2 Ferluti, former Tirana Factory, FIAT, the descent toward Lapraka; 11/3 Lapraka, Customs Directorate, Military Hospital, riverbank, Mëzes Field, Don Bosco.

Annex 2

Average Prices per Square Meter of Building Area for Non-Residential Buildings

a) The price per square meter of building area for commercial and service activities is 1.5 (one point five) times higher than the price of residential areas by city. This category also includes commercial buildings where mixed processes of production, trade, and/or retail services take place simultaneously. In areas within the Municipality of Tirana, this coefficient is 2 (two) times higher.

b) The price per square meter of building area for covered parking and basements is 70 (seventy) percent of the price of residential apartment areas by city.

c) The price per square meter of building area for open parking is 30 (thirty) percent of the price of residential apartment areas by city.

c) The price per square meter of building space intended for industrial activities, such as the production, processing, or storage of industrial goods, including factories, depots, warehouses and other similar facilities, is 50 (fifty) percent of the price of residential units in the respective area by city.

d) The price per square meter of building area used for agriculture and livestock or supporting activities, such as collection, storage, and preservation of agricultural and livestock products, is 30 (thirty) percent of the price of residential areas in the respective zone, excluding food processing.

d) The price per square meter of residential construction area in administrative units outside the respective city that joined the local self-government units after the entry into force of Law No. 115/2014, it is reduced by up to 35 percent compared to the price of the nearest zone, excluding residential areas. In the areas included in the Municipality of Tirana, this reduction is up to 30 (thirty) percent compared to the price of the nearest area.

e) For buildings privatized by Law No. 7652 of December 23.1992, “On the Privatization of State-Owned Apartments,” as amended, the price per square meter is 70 (seventy) percent of the price according to the table's zones, only in the case of the first sale.

Download

Source: Official Publications Center.