Relation

FOR

DRAFT LAW “ON AN AMENDMENT TO LAW NO. 8438 OF DECEMBER 28, 1998 “ON INCOME TAX”, AS AMENDED”

- The purpose of the draft law and the objectives it seeks to achieve.

Proposal of the draft law “On an amendment to the law" No. 8438, dated December 28, 1998, “On Income Tax”, ”as amended" is based on Articles 78, 83(1), and 155 of the Constitution of the Republic of Albania.

This draft law aims to:

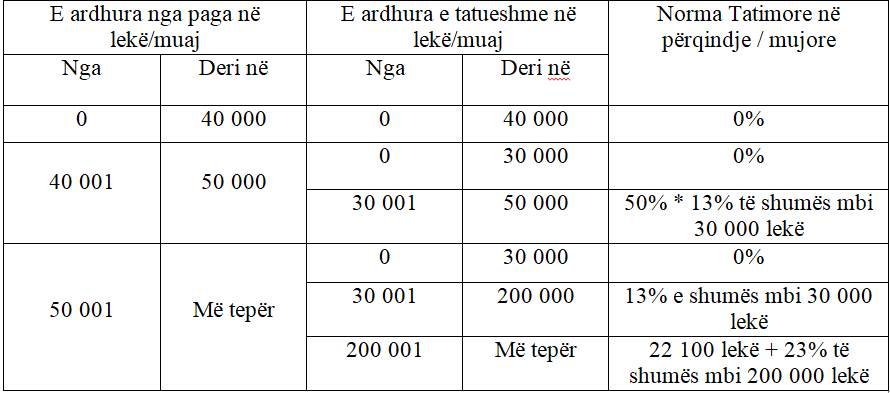

- Increase the non-taxable minimum wage for salary income in the range from 30,001 lekë/month to 40,000 lekë/month. For this pay range, the tax to be paid on wage income is 0%, allowing any citizen earning lower income to pay no tax on their wage income.

- Reduction of the tax rate by 50% for taxpayers with wage income from 40,001 lekë/month to 50,000 lekë/month. These taxpayers will pay 0% tax on up to 30,000 lek monthly wage income, and on the amount above that they will pay half the 13% tax rate (i.e., 50% * 13%). This ensures that lower-income citizens pay lower tax on their wage income.

- Supporting the middle class by revising the top bracket of progressive taxation. The 23% tax is expected to begin applying to salaries above 200,000 lek per month, up from the current 150,000 lek per month.

- Assessment of the draft act in relation to the Council of Ministers' political program, the analytical program of acts and other political documents.

This draft law is not included in the analytical program of draft acts to be submitted for review by the Council of Ministers during 2021.

- Rationale of the draft law regarding advantages, challenges, and expected effects.

This draft law has been prepared to fulfill the provisions set out in the government program, which emphasizes that every citizen who earns less income, will pay less income tax on their wages, but those who earn more will contribute more to the common welfare and also support the middle class.

In order to ease the tax burden on the most needy segments of the population, it has been proposed that taxpayers with personal income from employment in the range of 30,001 lekë/month to 40,000 lekë/month now pay 0.3% tax, instead of the 13% tax they paid on the amount above 30,000 lek/month. The number of taxpayers benefiting from the reduction of the tax burden is approximately 71,500, and the average benefit is 7,800 lek per taxpayer per year, or about 557 million lek per year for all taxpayers.

Also, in the same vein, to ease the tax burden on needy segments of the population, this draft law proposes that taxpayers with wage income from 40,001 lekë/month up to 50,000 lek/month, to continue paying 0% tax up to the amount of 30,000 lek/month of wage income, and, unlike the previous regime, on amounts above 30,000 lek/month they will pay half the 13% tax rate (13% * 50%). The number of taxpayers benefiting from this tax relief is approximately 58,000, and the average benefit is 11,700 lek per taxpayer per year, or a total of 678 million lek per year for all taxpayers.

As part of easing the burden on the middle class, this draft law provides for changing the top bracket of progressive taxation. The 23.1% tax is set to begin applying to salaries above 200,000 lek per month, up from the current 150,000 lek per month.. The number of taxpayers benefiting from this tax relief is approximately 5,900, and the average benefit is 23,000 lek per taxpayer per year, totaling 135 million lek for all taxpayers.

In total, the tax burden is reduced by 1.37 billion lekë per year for entities benefiting from the proposed changes in this draft law, which in turn translates into a corresponding loss of revenue for the state. Therefore, the implementation of these legal changes results in a negative effect on the state budget of -1.37 billion lek per year, while for 2022, since this forecast takes effect in July 2022, the negative impact for 2022 is projected to be -685 million lek.

- Assessment of legality, constitutionality, and harmonization with domestic and international legislation in force.

The draft law is based on Articles 78, 83(1), and 155 of the Constitution. Constitution.

- Assessment of the Degree of Conformity with the Community Acquis (for draft regulatory acts).

The draft law “On an amendment to Law No. 8438, dated December 28, 1998, “On Income Tax,” as amended” does not aim at aligning with European Union legislation (Community acquis).

- Explanatory Summary of the Contents of the Draft Act.

The draft law consists of two articles, which provide as follows:

Article 1 provides for the replacement of Schedule 1, “Table for Personal Income Tax on Employment,” of the law.

Article 2 provides for the law's entry into force.

- Institutions and bodies responsible for implementing this Act

The Ministry of Finance and Economy and the General Directorate of Taxes are charged with implementing this draft law.

- Persons and Institutions That Have Contributed to the Drafting of the Bill

The Ministry of Finance and Economy has drafted the bill. The bill is sent to the Ministry of Justice for review, to the State Minister for the Protection of Entrepreneurship, and, for information, to the State Minister for Relations with Parliament.

- Report on the Assessment of Revenue and Budgetary Expenditures

This draft law is expected to have a negative impact on the state budget of -1.37 billion lek per year. Meanwhile, for 2022, since this policy will begin to be implemented in July 2022, the negative impact on the state budget for 2022 will be approximately -685 million lek.

Source: Ministry of Finance and Economy.