Order 291, dated December 30, 2022

In support of Article 3, paragraphs 4 and 5, of Law No. 25/2018, “For accounting and financial statements”of the Council of Ministers“ Decision No. 505, dated July 17, 2019, ”On the approval of the internal regulations for the organization and functioning of the National Council of Accounting",

I COMMAND:

The issuance of amendments to International Accounting Standard No. 15 “On the Accounting and Financial Reporting of Economic Microentities (IAS 15)”.

This order takes effect upon publication in the Official Gazette.

Minister of Finance and Economy

Delina Ibrahimaj

Read below the full text of SKK No. 15.

Standard 15 “For the Accounting and Financial Reporting of Microeconomic Entities” Improved (Amended)

Tirana, January 20192022

Objective and Foundations of Preparation

- The Objective of National Accounting Standard No. 15 “For Accounting and Financial Reporting of Economic Micro-units” (SKK 15 as amended) as amended, approved by the National Accounting Council and promulgated by the minister responsible for finance, is to provide the basic concepts and principles and to establish the rules for applying these principles to the presentation of economic events in the financial statements of micro-entities.

- SKK 15 as amended is based on Law No. 25/2018, dated May 10, 2018. “For Accounting and Financial Statements.

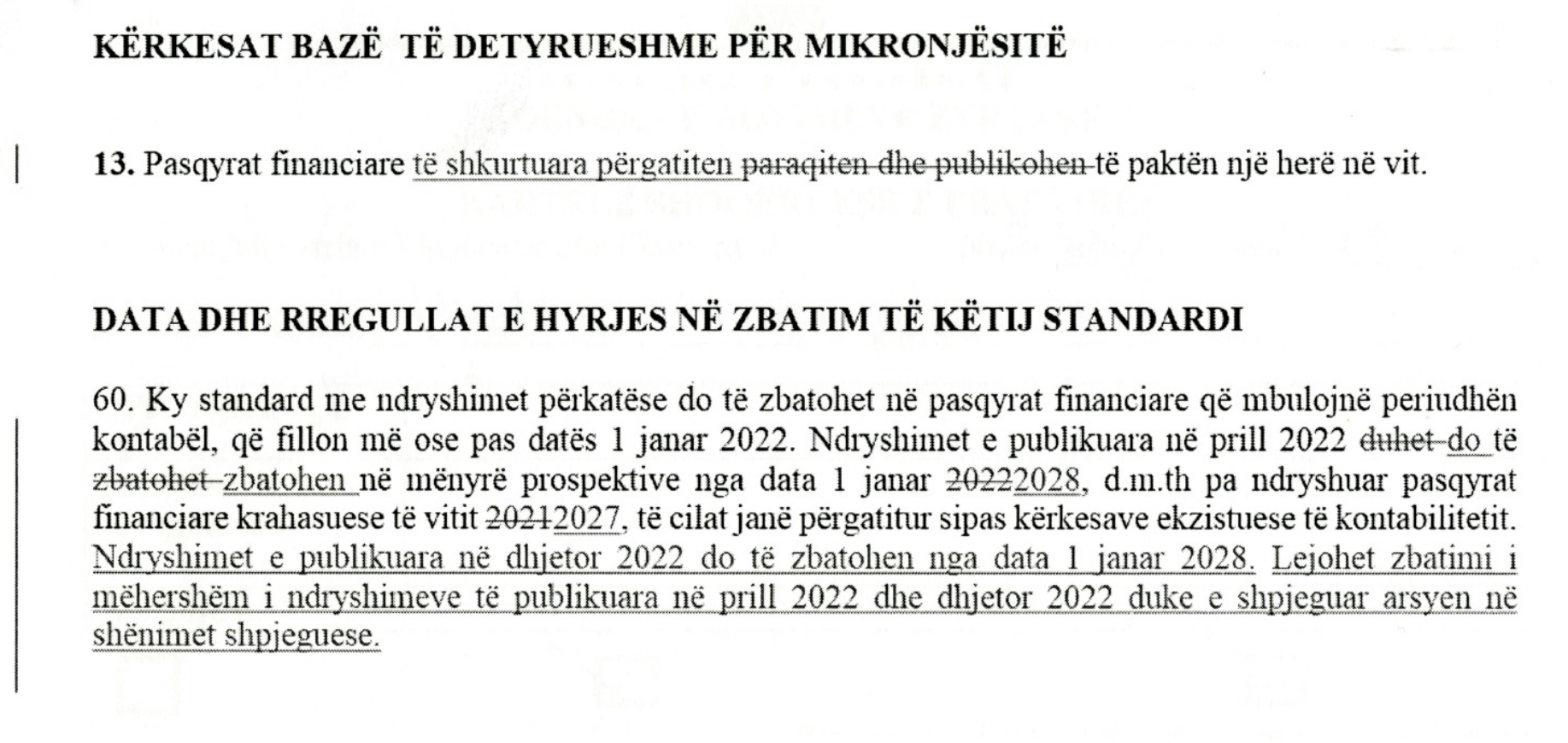

- This Standard focuses only on some of the basic issues concerning the organization of accounting, the keeping of accounts, and the preparation and presentation of simplified annual financial statements by micro-economic units.

- Financial statements will be prepared on the basis of the materiality concept, which implies giving importance to those aspects and financial data of economic activities that are significant to the users of the financial statements and that may influence the economic decisions they make. Overloading financial statements with excessive detail and immaterial information undermines their clarity and understandability. Financial statements are constructed based on underlying assumptions, principles, and characteristics of accounting information.

Field of Application

- This Standard shall be applied by all classified economic units. micronucléus from Law 25/2018 “For accounting and financial statements”.

Economic micro-units that generate no less than 5 million lek and no more than 30 million lek. Revenues from economic activity (turnover).

KEY DEFINITIONS

- Active is an asset or economic right controlled by the economic unit, which

- it has come as a result of past events; and

- Future benefits are expected from its use.

- Obligation is a current obligation of the economic unit, which

- was born from past events; and

- Its repayment is expected to be accompanied by future resource releases.

- Own Capital (or “net assets”) is the difference between the assets and liabilities of the economic unit as of the date of the statement of financial position.

- Income represent inflows (increase in economic benefits) during the reporting period that lead to an increase in assets or a decrease in liabilities, and that increase the economic entity's capital, excluding flows related to contributions from participants in capital.

- Expenditures represent outflows (reductions in economic benefits) during the reporting period that result in a decrease in assets or an increase in liabilities, and that increase the economic entity's capital, excluding flows related to contributions from capital participants.

- The assets, liabilities, and equity of the economic entity are presented in the economic entity's statement of financial position as of the reporting date.

12.Economic micro-units are economic units that, as of the reporting date, do not exceed the thresholds for at least two of the following three criteria: a) assets, 15 million lek; b) revenues from economic activity (turnover), 30 million lekë; c) average number of employees during the reporting period, 10. These criteria must be met for two consecutive years.- Value Depreciable The carrying amount of a long-term asset is the cost of the asset or another amount that replaces cost, less the asset's recoverable amount.

- Recoverable value It is the amount the unit expects to recover from an asset at the end of its useful life, after deducting the cost of disposal.

- Regular rent It is an agreement in which the lessor transfers to the lessee the right to use an asset for a specified period of time in exchange for one or more payments, without passing on to the lessee the risks and rewards associated with ownership of the asset.

- Financial asset is any asset that is:

- monetary tools

- a contractual right to receive monetary funds or another financial asset from another economic unit (for example, receivables);

- a contractual right to exchange financial assets with another economic unit on potentially favorable terms for the economic unit (for example, derivatives with a positive market value);

- an equity instrument of another economic unit (for example, investments in the shares of another economic unit).

- Financial obligation is the contractual obligation:

- to provide monetary funds or another financial asset to another economic unit (for example, a liability to a supplier);

- to exchange financial assets with another economic unit under potentially unfavorable conditions for that economic unit (for example, derivatives with a negative market value).

Objective of Microfinance Financial Statements

- The objective of the financial statements of economic micro-units is to provide information on their financial position and performance, which is used by users to evaluate, manage, and direct the micro-unit.

Users of Microcapital Financial Statements

- Financial statements are designed to reflect the needs of users. The primary users of micro-entity financial statements may be:

- Owners and operators;

- Lenders and other creditors;

- Government: For the purposes of micro- and macroeconomic planning;

- Tax authorities: For the assessment of tax liabilities;

- Micro-lending agencies: To assess the support requested by micro-units (e.g., grant applications, training requests, and business subsidy services).

Microenterprise Accounting System and Principles

- The financial statements of micro-entities subject to the application of this Standard shall be prepared on the basis of accrual accounting.

- The basic principles for constructing the financial statements of micro-entities are:

Principle of continuity – The preparation of the micro-entity's financial statements is normally based on the assumption that the business is ongoing and will continue to operate without any material changes for the next 12-month period, except in cases where the business activity is heading toward decline and its discontinuation or liquidation within the year, because there is no alternative course of action. If microentities choose to apply IFRS, they are permitted to do so, but their application must be made on a consistent basis.

The principle of non-compensationAssets with liabilities and revenues with expenses shall not be offset against each other, except in cases where such an offset is required or permitted by a national accounting standard.

- Under the rights and obligations method of accounting, the effects of transactions and accounting events are recognized in the financial statements when they occur (not when cash or cash equivalents are received or paid, as in cash‐basis accounting). Events and transactions are recorded in the accounting and reported in the financial statements of the accounting periods to which they belong. Financial statements, prepared on the basis of recognized rights and obligations, inform users not only about past transactions involving receipts and payments, but also about liabilities to be paid in the future as well as about assets that will generate future receipts. In this way, they present information on past transactions and events that best serve users in making economic decisions.

- Financial statements must be presented at least annually, as required by

Article 9 of Law No. 25/18, “On Accounting and Financial Statements”the Accounting Law. When the date for preparing the financial statements of an economic entity differs from the date prescribed in the Accounting Law, that is, when the annual financial statements are presented for a period longer or shorter than one year, the economic entity shall present, for the period covered by the financial statements, also the following information:- the reason for using a shorter or longer period;

the fact that the comparative amounts in the financial statements and the related explanatory notes are not entirely comparable with other periods.

Documentation and Maintenance of Microentity Accounting Records

- According to

Law No. 25/2018 “On Accounting and Financial Statements,” Article 7Under accounting law, accounting records are supported by accounting documents, in documentary or electronic form, that ensure their reliability. The accounting document is kept as documentary evidence for the entire period specified inArticle 8 of thisthis Law. For each accounting entry, the origin, nature, date, and content of the economic transaction or event must be recorded. Also, according to this Law,Article 23,The executive management body of the economic unit and its supervisory body, whether employees or not, are jointly and severally liable for fulfilling all requirements provided for in the provisions of this law. - Chronological entries are made in the journal. Microstructures may maintain a single journal or several journals. Systematic entries are made in the general ledgers and the subsidiary ledgers.

Characteristics of Accounting Information

- The qualitative characteristics of financial statements make the financial information presented in them highly valuable to users. The main qualitative characteristics are:

ComprehensibilityThe information in the financial statements should be presented in such a way that it is informative and unambiguous for those users of the financial statements who have sufficient knowledge of financial reporting to understand the financial statements.

Significance (materiality)In preparing financial statements, importance should be given to those aspects and financial data of economic activities that are material to the users of the financial statements and that may influence the economic decisions they make. Overloading financial statements with excessive detail and immaterial information undermines their clarity and understandability. Immaterial figures are presented grouped into categories with similar characteristics.

CredibilityTo be useful, information must be reliable. Information carries the quality of reliability when it is unbiased and free of material errors, and when users rely on it, trusting that it is a faithful representation of what it purports or is reasonably expected to represent. Information may be valid to present, but at the same time it may be so inherently or presentationally unreliable that its presentation could misinform the reader. For example, if the legal basis or the amount of a claim for compensation in a lawsuit is disputed, then it would not be appropriate for an economic unit to recognize the full amount of the loss in the statement of financial position, but, on the other hand, it would be appropriate for the amount and circumstances, regarding the loss, to be described in the explanatory notes.

ComparabilityConsistency in accounting policies and in the format of presenting financial statements is necessary for an objective comparison of the indicators of the economic unit's financial position and performance over the years. Standard requirements for accounting policies, formats for preparing financial information, and the information that must be presented in the financial statements form the basis for comparing the financial data of different economic units.

- The benefits derived from information must exceed the cost of providing it. However, the assessment of costs and benefits largely depends on management's judgment.

- In practice, it often happens that the qualitative characteristics of accounting information are in competition with one another. Determining the relative importance of these characteristics in different situations is a matter of professional judgment.

Basic Mandatory Requirements for Micronutrients

- The financial statements required from micro-entities, subject to the application of this Standard, are:

- Abbreviated statement of financial position;

- Abbreviated Statement of Income and Expenses (PASH);

- Abbreviated Explanatory Notes.

- Microentities subject to the application of this Standard are permitted to prepare additional statements in order to improve the transparency and quality of the information they present. (e.g., the statement of cash flows and/or the statement of changes in equity may be included).

- The annual financial statements present the following information:

- the name of the economic micro-entity and other identifying information, as well as any changes to this information from previous statements;

- the date of preparation of the financial statements or the accounting period covered by the financial statements, whichever is more appropriate;

- the currency for presenting the financial statements (lekes);

- the degree of rounding of the amounts presented in the financial statements.

- Financial statements are prepared and published at least once a year.

- The financial statements also include comparative data for the previous year. The values of the items in the financial statements at the end of the previous year are equal to the values of those items at the beginning of the following year.

- The micro-items present the elements in the balance sheet classified as current assets and non-current assets, current liabilities, non-current liabilities, and equity.

- An asset should be classified as short-term if it meets one of the following criteria:

- is expected to be realized or held for sale/consumption within the normal operating cycle of the business entity;

- is held primarily for trading purposes;

- is expected to be completed within twelve months after the date of the financial statements; or

- It is in the form of monetary instruments or a monetary instrument equivalent (as defined in IFRS 2, as amended), except when it is restricted to be used for settlement or to discharge an obligation for at least twelve months after the reporting date.

All other assets must be classified as long-term assets.

- A liability should be classified as short-term if it meets one of the following criteria:

- is expected to be paid off within the normal utilization cycle of the economic unit;

- is held primarily for trading purposes;

- The economic unit does not have any unconditional right to defer payment of the obligation for at least twelve months after the date of the statements.

All other liabilities must be classified as long-term liabilities.

- At a minimum, the financial position statement of the micro-entities shall include the items shown in Appendix 1 of this Standard.

- At a minimum, the income and expense statement includes the items shown in Appendix 2. Appendix 3 provides a more detailed presentation but with the same structure.

- In the statement of financial position or in the statement of income and expenses, other items that are important and material to the micro-entity may be added.

Recognition

- Recognition is the process of including in the financial statements an item that meets the definition of an asset, liability, revenue, or expense and that satisfies the following criteria:

- It is possible that any future economic benefit related to this item will flow to or from the economic unit; and

- The voice has a cost or value that can be measured reliably.

- An asset or liability is recognized only when the entity becomes bound by the contractual terms of the financial instrument.

- Rent payments are recognized as expenses at the time of payment. If payments for subsequent periods are material, they must be disclosed in the notes to the financial statements.

- The value of leased assets is not reflected on the lessee's statement of financial position., Neither as an asset nor as a liability. For micro-units there is only one type of lease: the standard lease. Therefore, every lease agreement, regardless of its contents, for a micro-unit will be recognized as a standard lease, whether the unit is the lessee or the lessor.

- Revenue from the sale of goods is recognized at the point of transferring the risks and rewards of ownership of the sold assets to the buyers.

- Service revenues are recognized in proportion to the services rendered, using the stage-of-completion method.

Measurement and Subsequent Evaluation

- The initial measurement of assets and liabilities is made only using the historical cost model.

- Historical cost for long-term tangible and intangible asset items means the purchase price, including port charges and non-refundable taxes, as well as any other direct expense incurred in bringing these assets in and placing them in working condition.

- The depreciable amount of AAM and AAJM is expensed in the respective annual periods based on their useful lives. The simplest method is linear depreciation, but any other method that results in an equitable allocation of the depreciable cost to the cost of the reporting periods may also be used. Land normally has an indefinite useful life, therefore it is not depreciated. Buildings have a defined useful life, therefore they are depreciable assets.

- The initial measurement of inventories at historical cost includes all purchase costs and other expenses that serve to bring the inventories to the location and condition for use (e.g., transportation costs).

- Tracking inventory levels is done by the specific identification method of individual costs for each item, when possible. Otherwise, it is done using the FIFO method or the average cost method.

- In the statement of financial position, tangible or intangible long-term assets are presented at cost less depreciation.

- On the statement of financial position, inventories are presented at cost.

- Financial assets and liabilities are presented in the statement of financial position at cost or their amortized cost.

- At the end of each reporting period, an economic unit must:

- to translate monetary amounts expressed in foreign currency using the closing date exchange rate of the statements;

- to translate non-monetary amounts into foreign currency using the exchange rate on the transaction date.

- The year's profit or loss is presented as a separate item in the statement of financial position.

- The income tax expenses shown in the income and expense statement are those calculated on the period's taxable profit.

Explanatory Notes

- In the explanatory notes to the financial statements, explanations must be provided for each grouping of AAM and AAJM items regarding the opening and closing balances, showing:

- Add-ons;

- Out-of-service exits;

- Depreciation; and

- Other movements.

- The explanatory notes to the financial statements also include:

- The description of the micro-entity's activity and its primary activity.;

- References to the accounting standards used to prepare the financial statements;

- Explanations of inventory accounting policies;

- Explanations of contingent assets and liabilities;

- Any other important information for understanding the financial statements.

- For material transactions or accounting actions and treatments not addressed in this Standard, the explanations provided in other improved IFRSs may be used.

Dates and rules for implementing this standard

60. This standard, with the relevant amendments, shall be applied to financial statements covering the accounting period beginning on or after January 1.

20192022.This standardThe changes published in April 2022 must be applied prospectively as of January 1.20192022, i.e., without changing the year's comparative financial statements.20182021, which have been prepared in accordance with existing accounting requirements.

Model of Financial Statements for Economic Microniches

1. Financial statements

Accounting and financial statements may be maintained and prepared by micro-entity employees who hold a degree in economics or by external accountants under a service contract. The report formats take into account issues related to the cost/benefit analysis for micro-units. In order to ensure that the reports are useful to owners-managers and other users of the financial reports, the cost of preparing the financial reports is assessed in relation to the benefits of their preparation. The objective of the financial statements is to help owners–managers obtain valuable information for business development. They also help other users make decisions and monitor the micro-entity's progress. Therefore, the design of these reports must meet the needs of the users.

The PF formats attached to this standard are mandatory. Microunits may add PF line items based on the principle of materiality and the provision of true and fair information, but they may not reduce the main line items.

B. Statement of Financial Position – Appendix 1

The table presented is the mandatory format for the statement of financial position. It includes the main items as well as the contents of these items, presented separately under other sub-items. While the main items, presented in black type, are mandatory, other sub-items may be added or removed depending on the nature of the micro-entity's activities.

C. Statement of Income and Expenditures – Appendices 2 and 3

The first format presented in Appendix 2, he according to nature, It is the mandatory format for the income and expense statement. Depending on the micro-entity's activities, it may be appropriate to modify the content of these line items or add other sub-items.

The second format presented in Appendix 3, it according to function, It is not mandatory to implement, but its preparation is encouraged for management purposes, since the structure of the income and expense statement is primarily designed to meet the needs of the owners–managers. This statement is used by them to verify whether they have accurately projected cost levels and profit margins in their selling prices.

Direct operating expenses vary from one micro-entity to another. For example, Appendix 3 illustrates an overview of revenues and expenses for a retail micro-entity, where margin is calculated on purchases. Other types of micro-units may use different allocations for the direct costs of operating activities. Most micro-unit expenses are direct expenses.

D. Statement of Cash Flows – Appendix 4 (a/b)

The primary objective of the statement of cash flows is to provide clear information about the movements of cash flows of the microentities during a specified period. Although this statement is not required by this Standard, Appendix 4 presents two models of the statement of cash flows according to the method used (4/a direct method and 4/b indirect method)..

Download

Source: