1. Any employer who is obligated to pay income from employment is required to withhold tax on this income, to submit the payroll list and transfer the tax withheld on the payroll list to the budget treasury account no later than the 20th of the following month for entities and no later than the 20th day of the month following each quarter for self-employed individuals or sole proprietors. and self-employed individuals or traders registered for VAT, and no later than the 20th of the month following each quarter for self-employed individuals or traders who are not registered for VAT.

(Amended by Normative Act No. 7, dated December 14, 2023, published in the Official Gazette) No. 182, December 16, 2023

The payroll tax agent is required to withhold tax in accordance with this provision:

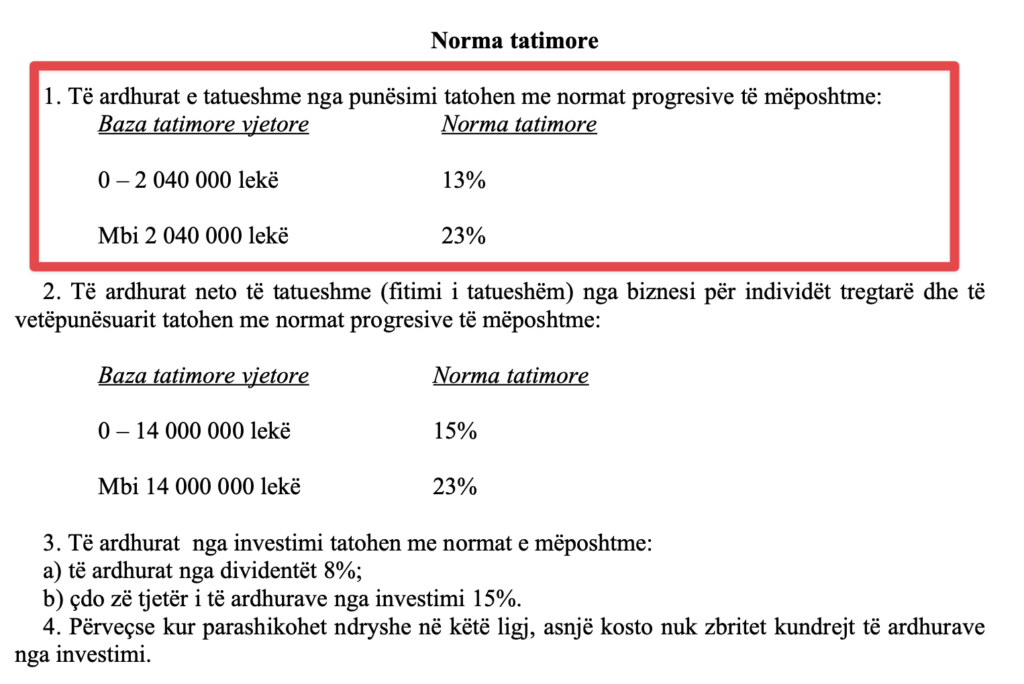

a) the progressive rate of taxation under Article 24 of this law if the personal income taxpayer signs the declaration of personal status with this employer, pursuant to Article 64 of this law;

“…Article" 24

b) 15% of the payment in other cases not covered by paragraph (a) of this point and not considered income from employment relationships.

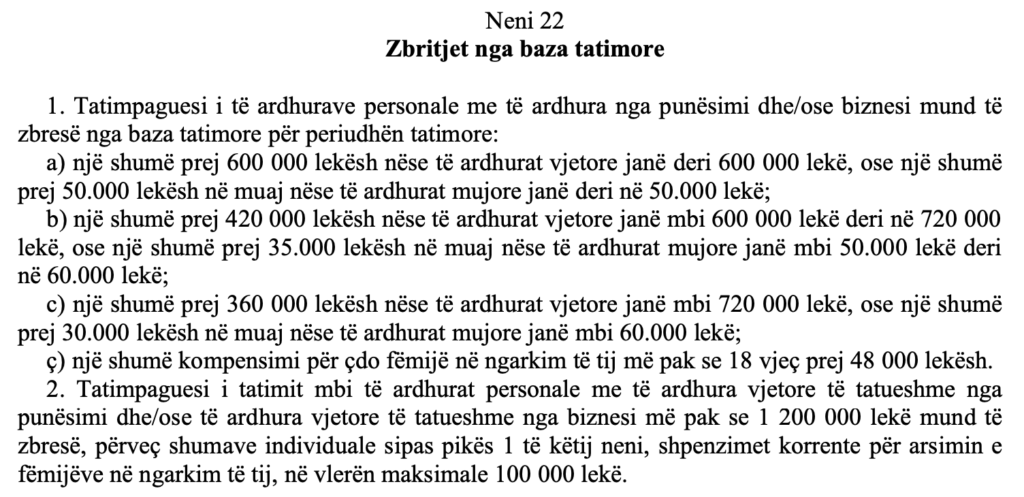

The payroll tax agent is required to take into account, on a monthly basis, one-twelfth of the deductions from the tax base, in accordance with letters “a,” “b,” and “c” of paragraph 1 of Baby 22 of this law, and the deductions from the tax base under Article 20 of this law when calculating the income tax on the payroll for an employee who has signed the personal status declaration with this payroll tax agent. If the employee is also employed by other employers, those other employers, in their capacity as payroll agents, will apply the progressive rate of taxation under Article 24 of this law and will not apply the deductions from the tax base under Baby 22, point 1, letters “a”, “b” and “c” of this law.

“… Article 22

2. Deductions and offsets under points 1, letter “ç”, and 2 of Baby 22 and according to Article 23 Under this law, they may only be claimed by personal income taxpayers on the annual tax return.

4. Payroll tax agents are responsible for paying employment income taxes with the same responsibility as if they were their own tax liability.

3. Every employer must keep records of the income paid and the tax withheld and submit the payroll in accordance with the provisions of the tax legislation and the legislation on social security and health insurance contributions, as well as the instructions issued by the minister responsible for finance for the implementation of these laws. The form, content, deadlines, and procedures for submitting the payroll register are determined in the secondary regulations of the minister responsible for finance, issued for the implementation of the tax legislation, including this law, as well as the legislation on social security and health insurance contributions.