Changes latest The law on statutory auditing marks a significant step towards modernizing the practice and complying with international standards. This law brings an increased focus on transparency, professionalism, and harmonization with global requirements, affecting several key areas of this profession.

In this article, we will analyze the most significant changes and their impact in practice.

The Importance of Legal Changes

The latest revision of the law aims to:

- To empower professional organizations and auditing firms to meet new standards.

- To increase the quality of training and testing of new auditors.

- To clearly define economic entities required for statutory audit.

- To establish clearer rules for how auditing firms are organized.

Changes for Audit Organizations and Firms

Expansion of Professional Organizations' Responsibilities

Professional organizations of statutory auditors (IKEAalready have a more active role in training auditors on sustainability reporting and aligning practices with international standards for non-financial reports.

Public Register Update

The information public registry for statutory auditors and audit firms now includes: (a) Approved status of auditors for sustainability reporting. (b) Information on competent authorities for supervision and quality control.

Quality Control

Public Oversight Board (POB) It has taken on new responsibilities, including delegating quality control for non-public interest entities to professional organizations and maintaining general oversight to ensure standards.

Training of Legal Auditors

Structured Professional Practice

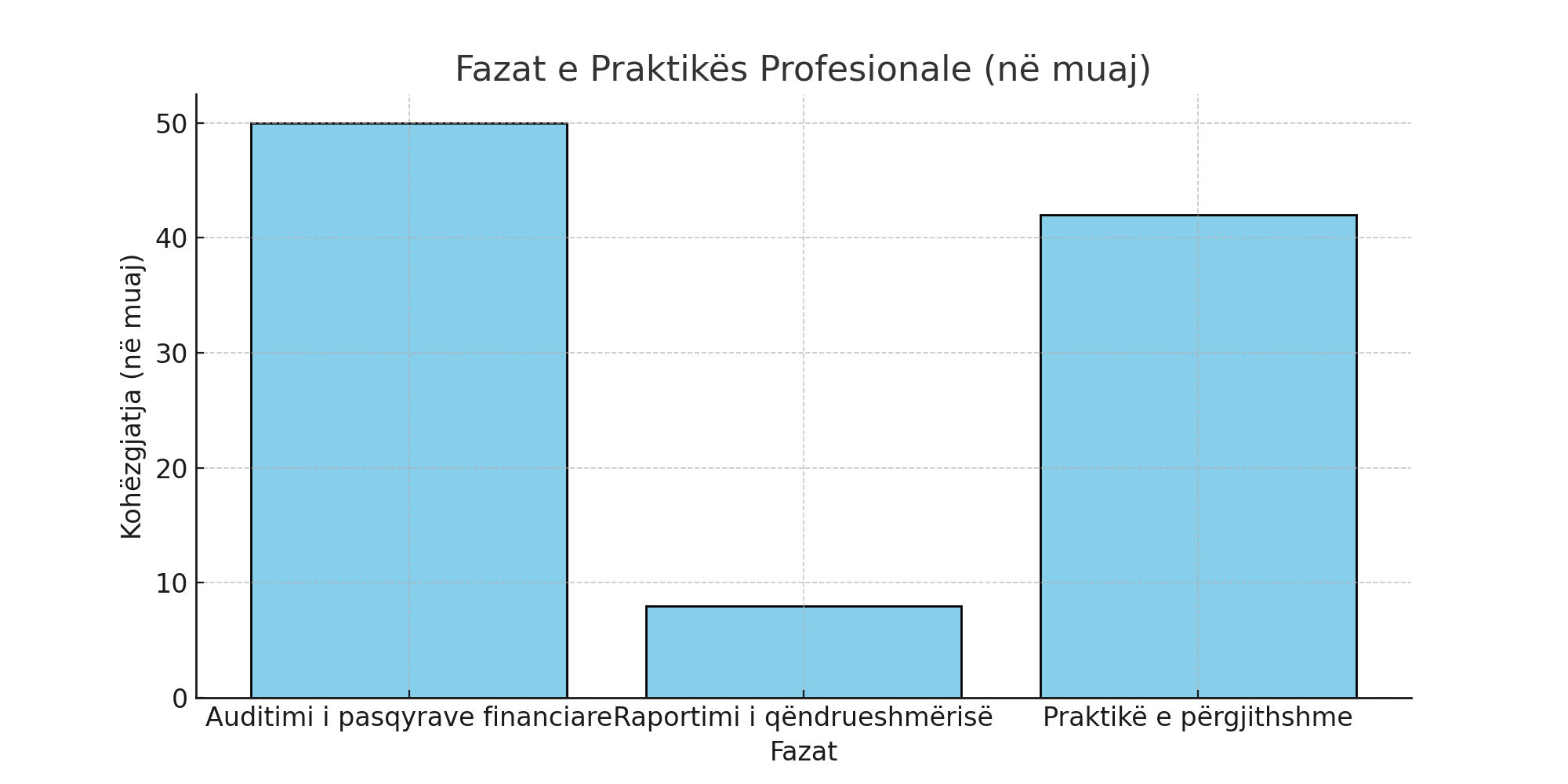

New auditors must meet specific requirements during their three-year professional practice:

- Half of the time should be focused on auditing the annual and consolidated financial statements.

- Eight months are dedicated to sustainability reporting.

- The majority of the internship must be completed with a recognized and registered auditor in Albania.

Exclusions Review

Individuals with international titles such as Certified Public Accountant apple Acca are no longer excluded from professional practice, ensuring equal standards for all candidates.

Professional Exams

Increasing New Disciplines

The examination program now includes knowledge of sustainability reporting legislation, analysis, and due diligence processes for sustainability issues.

International Harmonization Test

Candidates with foreign certifications must pass additional tests to demonstrate their knowledge of Albanian regulations and relevant standards.

Legal Audit Criteria

Determination of Auditable Units

In addition to public interest entities, legal auditing is also required for entities that meet two of these three criteria:

- Assets over 50 million lek.

- Annual income over 100 million lek.

- More than 50 employees on average during a year.

Rules for Audit Firms

Appointment of Principal Partners

Auditing firms must appoint a key partner for sustainability audits. This individual must meet the criteria for professional independence and have sufficient resources and staff to carry out the tasks effectively.

Customer and Service Registration Records kept by audit firms must now include: (a) Detailed client information. (b) Fees applicable to services rendered, and (c) Detailed documentation on audit and assurance processes.

Conclusion

Changes in the statutory audit law represent a significant step towards modernizing this profession and adapting to global demands. These improvements not only increase transparency and accountability but also provide a stronger foundation for the professional development of statutory auditors and audit firms in Albania.

Download Legal Change