Who Are We?

Alprofit Consult is an independent studio that provides accounting services, tax administration services and financial consulting services along with training services in these fields. We offer a full package of personalized professional services to businesses and individuals who wish to benefit from these services.

At AlProfit Consult, we are committed to ensuring that our clients have the resources they need to optimize their financial position and business operations. We welcome the opportunity to learn more about your financial service needs and how we can assist you.

We also invite you to benefit from our offer of providing financial consulting services free of charge for the first month. We would be very willing and interested to organize a meeting and discuss your ideas and projects in more detail. Please do not hesitate to write to us with any questions.

Main Laws for Business Registration and Administration

Albania has taken rapid steps in aligning its legislation with the requirements and conditions for accession to European organizations. Its acceptance as a candidate country is expected soon, and the reports prepared for this purpose have identified significant progress made by Albania in this field.

The main laws that directly affect the operation of commercial companies in Albania are as follows:

Law no. 9723, dated 03.05.2007 “On the National Registration Center” (most recently amended to the National Business Center).

This law, together with the legal framework in this field and the related by-laws, represents one of the most important and successful steps for the operation of commercial companies and sole proprietors. The National Business Center (NBC) is the only institution responsible for business registration in the commercial register. Registration at the NBC counters, through a one-stop-shop system, is sufficient for the simultaneous registration of the commercial entity with all other related institutions (Municipality for local taxes, Tax Authorities for taxes payable, Social Insurance Institute for employees, etc.).

- The application form at the NBC. This is the form completed at this institution where the company’s details are declared.

As of May 2022, all initial registration services and amendments at the National Business Center are carried out ONLY online.

- The company statute, which defines the company’s details (Name, Form – limited liability company, date of establishment, identification details of the founders, registered office, scope of activity, duration – if specified, administrator details, value of the share capital – minimum 100 ALL). This document does not need to be notarized.

- Authorization of the person who will perform the business registration (if different from the company administrator). This document must be notarized.

Commercial companies must also publish in the commercial register any changes defined by this law, in addition to the initial registration.

Law no. 9901, dated 14.04.2008, “On Entrepreneurs and Commercial Companies”, together with the related legal acts.

This law primarily defines the forms of organization of commercial companies and the manner in which they are administered/governed by the company’s own bodies. The law aims to establish the framework for business organization and, depending on the form of the business, the bodies that the registered business must establish, their rights and obligations, decision-making processes, etc.

In accordance with the requirements of this law, the company defines and approves its statute, appoints the administrator, establishes other company bodies, the shareholders’ assembly, profit distribution, etc. The law incorporates best practices in this field for the protection of shareholders, creditors, and corporate governance in the future.

Main Taxes Applied in Albania

Albania has taken significant steps to implement a simple tax system, encouraging the spirit of self-declaration and self-calculation of taxes by taxpayers. Despite issues related to instability in fiscal legislation and frequent amendments to laws and by-laws, the tax burden applied to taxpayers and the taxes in Albania remain among the lowest in the region and represent an advantage for attracting foreign investment. The main taxes applied in the Republic of Albania are briefly as follows:

Income (profit) tax

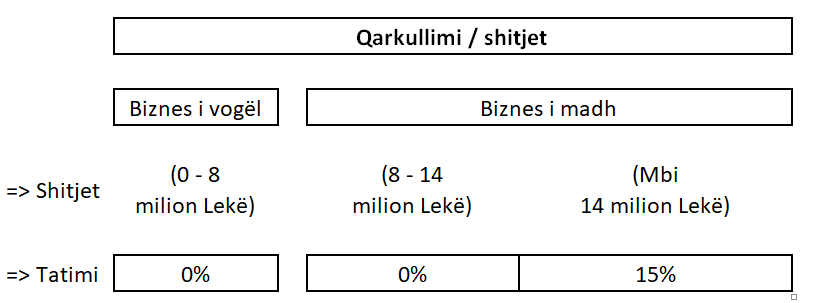

Profit tax is paid on the calculated and declared profit of companies and other entities in proportion to the taxable profit. In Albania, for profit tax purposes, the law classifies commercial entities into two groups, according to the following scheme.

- Large businesses, subject to income tax. The law classifies this category into two subcategories; (i) Entities with turnover up to 14 million Lek (or approximately €110,000) that calculate and pay income tax at a rate of 0% on taxable profit, and (ii) Businesses with revenue over 14 million Lek (or approximately 110,000 Euro), which are taxed at a rate of 15% on taxable profit. Large businesses are considered those entities that exceed the turnover (sales) threshold of 8 million lek (or approximately 65,000 euros) per year. These entities file their profit tax returns once a year by March 31 of the following year.

- Small businesses are subject to the simplified profit tax. Entities with annual turnover from 0 to 8 million lek calculate and pay the simplified profit tax at a rate of 0.1% on taxable profit. The deadline for filing the declaration for this category is February 10 of the following year.

Taxable income is determined by the accounting profit of the period, adjusted for income tax purposes with certain specific exceptions related to the documentation of tax expenses and the purpose of incurring these expenses in the function of the company's activity.

Tax payment is made by pre-paying monthly tax installments, based on the amount of tax paid in the previous year. If at the end of the fiscal period, the entities have a larger profit, the difference is paid by completing the annual profit tax return. Otherwise, any overpayment is either refunded or carried over to pay future tax liabilities. In this area, the law allows entities to estimate their taxable profit and justify to the tax authorities their request for a reduction in advance profit tax installments.

All other income is taxed at a rate of 15%, except for dividend income, which is taxed at a rate of 8%. This includes all other income not covered by the two categories above. For example, rental income is taxed at the rate of 15%.

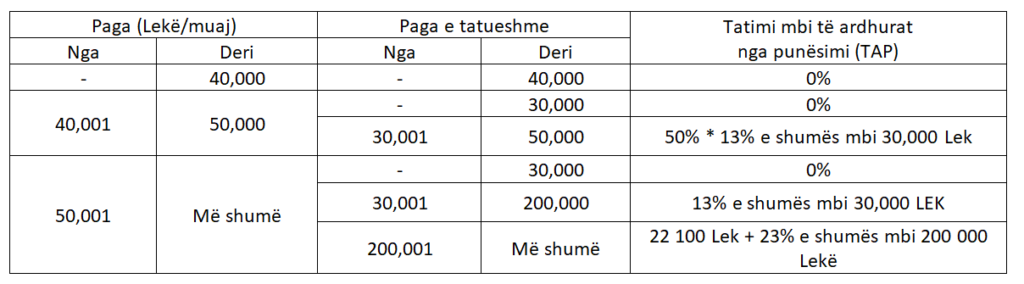

Employees are also taxed on income from a salary (TAP), which is calculated based on gross salary and a progressive tax rate as follows.

The income tax is paid by the employee, and this tax is collected by the employer.

Value Added Tax (VAT)

The standard VAT rate in Albania is 20%. A reduced VAT rate of 6% applies to the accommodation and agriculture sectors. The VAT registration threshold is an annual turnover of 10 million ALL. Any entity may voluntarily register for VAT purposes even if it does not meet the turnover requirement, through a simple request to the tax authorities. VAT applies to the supply of goods and services to taxable persons in the Republic of Albania.

VAT returns are filed monthly, and the payable amount is calculated as the difference between VAT collected on sales and VAT paid (credited) on purchases. Recent legal changes provide relief and time limits for VAT refunds. VAT may be refunded if the VAT credit balance exceeds 400,000 ALL for three consecutive months.

Social and Health Insurance Contributions

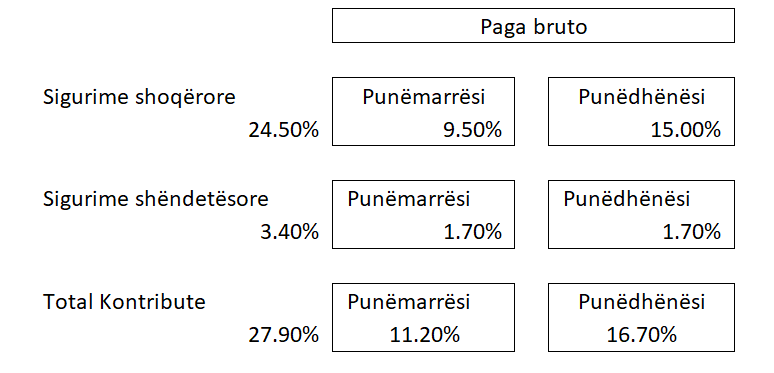

Social and health insurance contributions for company employees are calculated based on gross salary and applicable contribution rates. For each employee, the employer calculates and withholds the employee’s contributions from monthly salary, as well as pays the employer’s contributions.

Employee contributions are: Social insurance: 9.5% of salary, Health insurance: 1.7% of salary Employer contributions are: Social insurance: 15% of salary, Health insurance: 1.7% of salary

Social security contributions are applied to the base salary for the current minimum of 32,000 Lekë and a maximum of 141,133 Lekë. For salaries above the maximum wage, social security contributions are applied to the wage of 141,133 Lekë. The sum of social security and health insurance for the minimum wage is 8,928 Lekë.

Local Taxes and Fees

Mandatory tax payments also include local taxes and fees payable to local government (municipality). Generally, local taxes and fees are paid once per year and are calculated based on specific criteria.

The average payable amount for most businesses registered in the city of Tirana ranges from 10,000 to 50,000 ALL per year.

Download the full information here.

Source: AlProfit Consult.