The VAT credit balance is the difference between the VAT calculated on supplies made by the taxpayer and the VAT deductible on supplies received by him during a tax period.

Taxpayers who have a VAT credit surplus may request a refund under the conditions set forth in the Law. “For VAT” and procedures in The instruction of the Minister of Finance.

The emergence of the right to refund VAT credit surpluses

Taxpayers have the right to request a VAT refund when:

1. to have carried a credit balance for three consecutive months and

2. The amount of VAT requested for refund is greater than 400,000 lekë.

For exporters, the number of tax periods for which they have a credit surplus is not a requirement; only that the surplus exceed 400,000 lekë.

Deadlines for processing VAT refunds

- For exporting taxpayers, within 30 days from the date the request is submitted.

- For taxpayers not classified as exporters, within 60 days from the date the request is submitted.

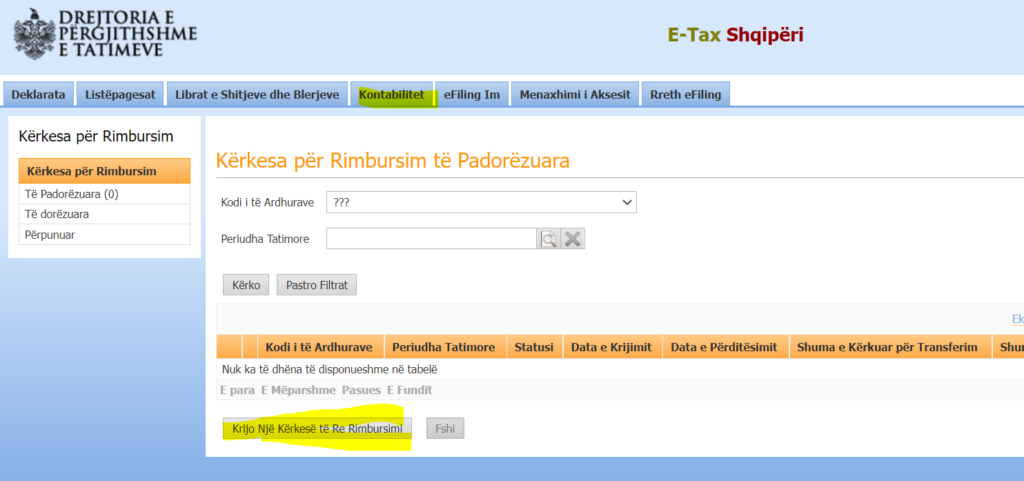

Reimbursement Request Form

The taxpayer must electronically complete the “Request for Refund,” displayed in the “Accounting” submenu, through his account in the tax system. Next, the taxpayer must click on the “Create a New Refund Request” link to proceed with filling out the required form.

Once completed, it must be printed and mailed to the VAT Reimbursement Directorate at General Directorate of Taxes.

Preliminary verification of reimbursement requests

The taxpayer's request for a VAT credit surplus refund is subject to a preliminary verification process regarding:

- The conformity of the amount requested for reimbursement on the “Reimbursement Request” form with the amount of deductible VAT as shown on the taxpayer's account.

- The fulfillment of the legal criteria for reimbursement, which relate to:

- Verification, if the excess of the deductible VAT claimed for refund exceeds 400,000 lekë, for exporting taxpayers;

- Verification, if it results in deductible VAT for each of the three consecutive periods, the sum of which after these three periods must exceed 400,000 lekë, for other non-exporting taxpayers.

Receipt of reimbursement request

When the preliminary verification process of the refund request shows that the criteria have been met, the request is considered accepted. The taxpayer is officially notified of this via the appropriate form approved for that purpose, and the Treasury Department is also informed.

- In the event the refund request is approved, within five business days from the date the administration receives the request, the taxpayer will receive the document “Notice of Approval of VAT Refund Request.”.

- At the same time, this document informs the taxpayer that the VAT refund will be carried out according to a procedure based on a risk analysis for refunds.

Analysis of the risk of reimbursement claims

The way refund requests are handled may vary depending on the level of risk and the amount of VAT requested for refund.

- If the taxpayer is a zero-risk exporter, the refund request is not subject to refund risk analysis and the refund is processed automatically.

- If the taxpayer is not a zero-risk exporter, but the value of exports carried out in the tax period(s) for which the refund is requested represents more than 50% up to 70% of the total sales value, including exports, are refunded within 30 days from the date the VAT refund application is filed, subject to prior risk analysis.

- If the taxpayer is not an exporter, the refund is issued within 60 days from the date the refund request is filed, subject to the risk analysis procedure.

- Refund requests that, after analysis, are deemed risk-free are approved for automatic refund of the requested amount, without conducting a taxpayer audit before VAT refund approval.

Rejection of the reimbursement request

When the preliminary verification of the refund request shows that the criteria have not been met, the request is considered irregular and is not accepted. In this case, the taxpayer is officially notified using the appropriate form approved for this purpose.

The taxpayer may submit a new refund request under the above rules only after correcting the situation and eliminating the reasons why the previous request was denied.

Refund requests that result in risk

If the reimbursement request is found to be at risk of fraud, the VAT Reimbursement Directorate at the DPT sends it to the regional directorate where the taxpayer is registered for:

- office inspection or

- On-site inspection before reimbursement.

The audit procedure is carried out as provided for in Law No. 9920 of May 19, 2008, on Tax Procedures in the Republic of Albania, as amended.

Deadlines for completing the inspection

- In the event that the taxpayer is subject to a tax audit, the deadline for the inspector(s) to complete the audit report is no more than five calendar days after its conclusion.

- The deadline for the taxpayer to contest the results of a tax audit is no more than five calendar days after the date on which the audit report is deemed to have been received.

Payment of the approved reimbursement amount

After the VAT amount to be refunded is approved, the refund payment order is completed. (UPR) with the amount of VAT to be refunded is completed and sent to the treasury branch, which pays the refundable VAT amount within 5 days from the date the payment order is submitted by the VAT Refund Directorate to the DPTs.

For more information, click on www.tatime.gov.al, go to the taxpayer service counters at any Regional Tax Directorate, or call the toll-free number 0800 00 02 of the Call Center at the General Directorate of Taxes.

Source: General Directorate of Taxes.

Download here and below the information card.