Part of the changes of The new income tax law, It also includes the personal income tax on employment. These changes take effect for the period beginning June 2023 and thereafter. They are part of other changes to the way individuals are taxed and of the minimum wage increases.

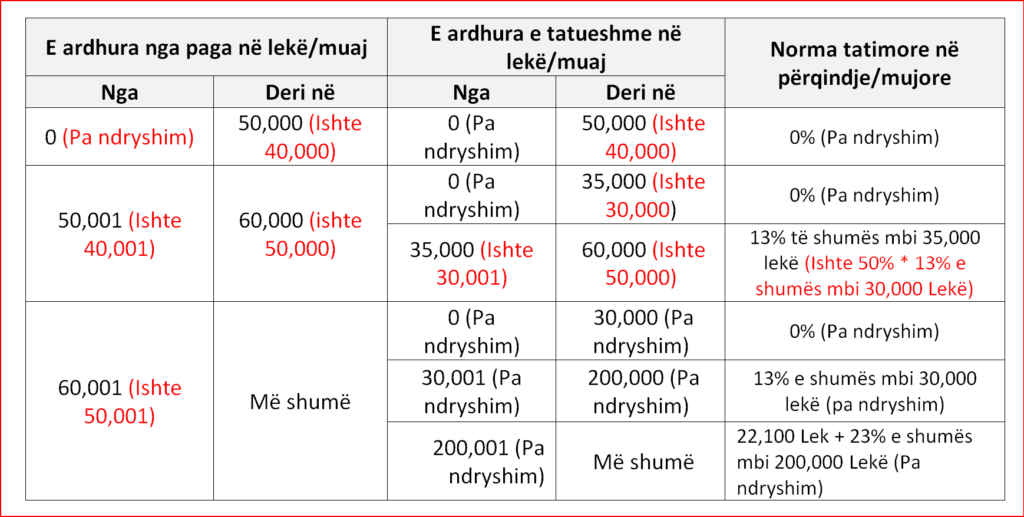

Essentially, the scheme remains the same: progressive taxation divided into several tiers (0 – 50,000 Lek; 50,000 – 60,000 Lek; and over 60,000 Lek). The new scheme and comparisons with the old scheme are presented below.

The first change is that the taxable wage threshold has been raised from 40,000 Lek to 60,000 Lek. This means that for salaries below 60,000 Lek per month, the income tax rate on employment income will be zero.

The other change is the adjustment of the middle bracket from 50,000 to 60,000 Lek, where the non-taxable threshold has also been raised from 30,000 Lek to 35,000 Lek. But it is accompanied by an increase in the tax rate for the 35,000 to 60,000 Lek range, from a 50.1% rate on the amount above the threshold (the revised 35,000 Lek) to 13.1%.

Meanwhile, the tax on third-level income, apart from raising the threshold from 50,000 Lek to 60,000 Lek, remains unchanged.

The changes affect the non-taxable wage threshold and up to 60,000 Lek/month. The portion of wages above 60,000 Lek/month will have no effect on tax calculation.

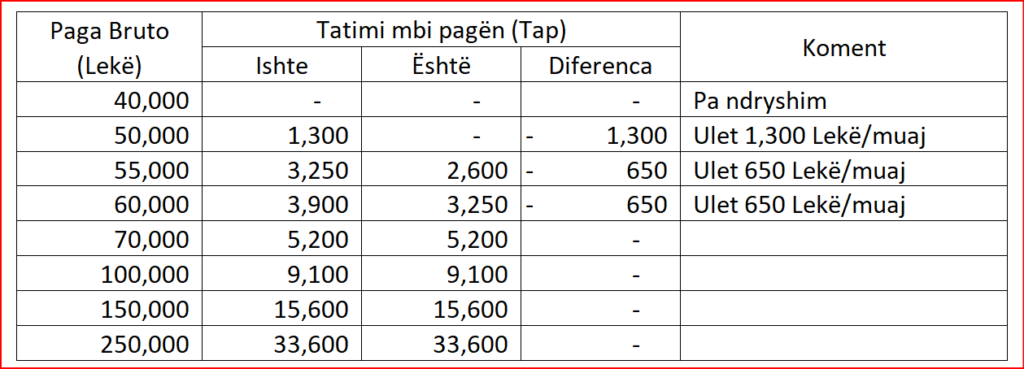

The table below also shows the tax changes for different pay levels.

Read the full law as well. here .

Download below a simplified Excel file for the automatic calculation of the income tax rate on employment income for different gross wage levels, before and after legal changes.